Quantifying the COVID Impact

2020 was the most challenging year on record for hotel owners, far surpassing the lows reached following the 2008 and 1981 recessions. In order to project how and when hotels will recover, we believe it is worth separating the recession’s purely economic impacts from the “stay home” COVID impact.

Historically, estimating hotel performance has been easier than one might think. Using only hotel construction completions and employment changes, for instance, we were able to model1 74% of annual revenue per available room (RevPAR) growth within a given year, from 1992-2019 (See figure 1). The relationship obviously disconnected in 2020 as the pandemic began.

Specifically, RevPAR declined by 47.5% in 20202, but the above model suggests only 3.5 percentage points of the decline can be attributed to typical demand factors (i.e. employment declines) and supply coming online (see figure 2). We attribute the remaining 44.0 percentage points to the COVID-related demand impact, driven by social distancing and stay home orders, and we believe this gives us a reasonable starting point from which we can forecast the post-covid recovery in hotel demand and thus RevPAR.

Hotel Demand in a Post-COVID World

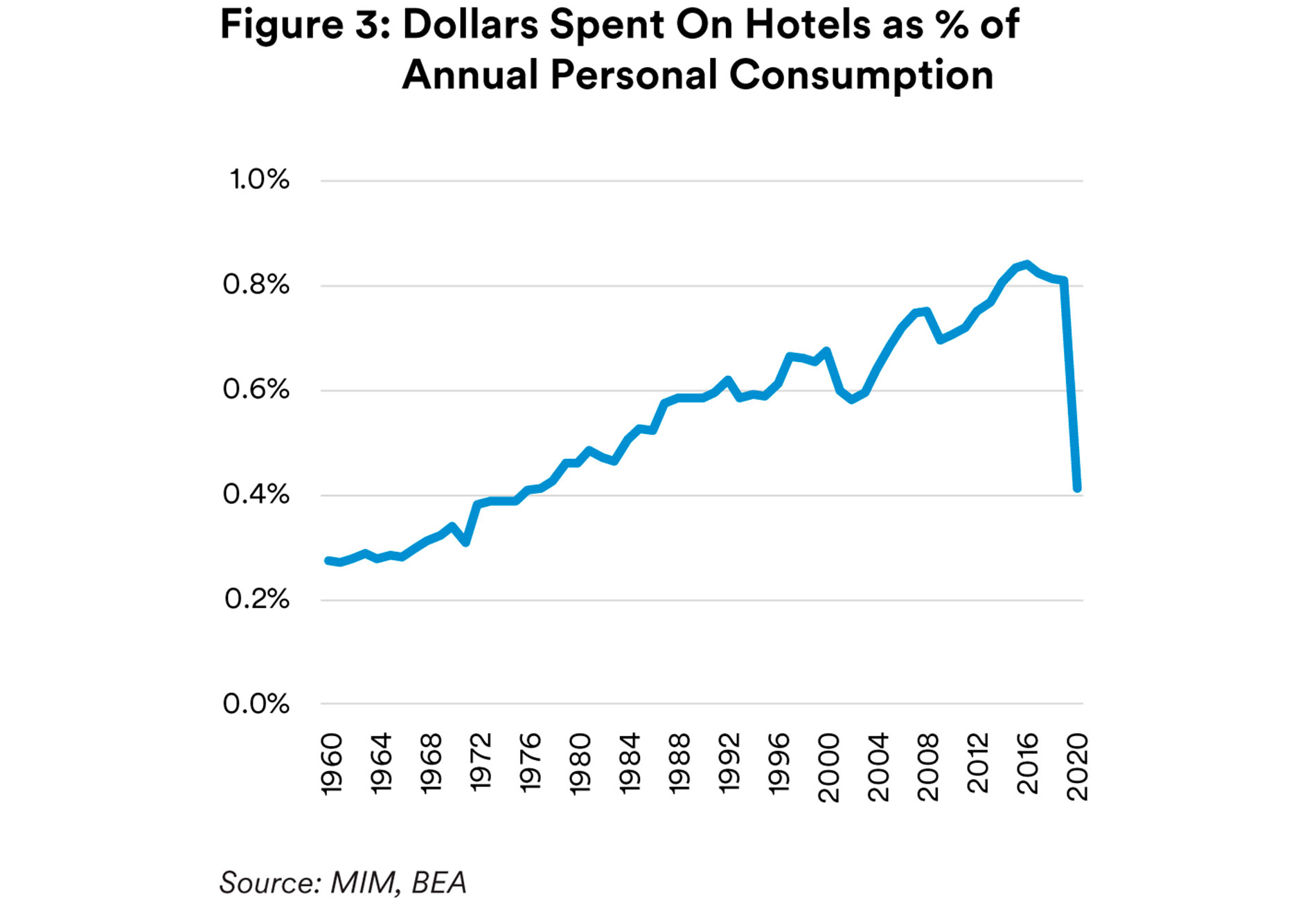

As we noted in a 2019 report, A New Dawn in Retail, experiences (versus goods) are capturing an increasing share of personal expenditures, and hotels have benefited from this trend over the past several decades. As seen in figure 3, even following the introduction and rapid expansion of a major competitor (Airbnb) in the last decade, hotels’ share of personal consumption has steadily increased. We do not believe the pandemic has altered the secular shift toward experienced based spending.

In addition to consumer preferences favoring experiences over goods, the nature of this downturn suggests that those who are most likely to spend on travel will have the means to do so once vaccines are widely distributed and travel is considered safe. Our base case assumption is that vaccine distribution will allow for herd-immunity to be achieved in the U.S. by mid-summer.3

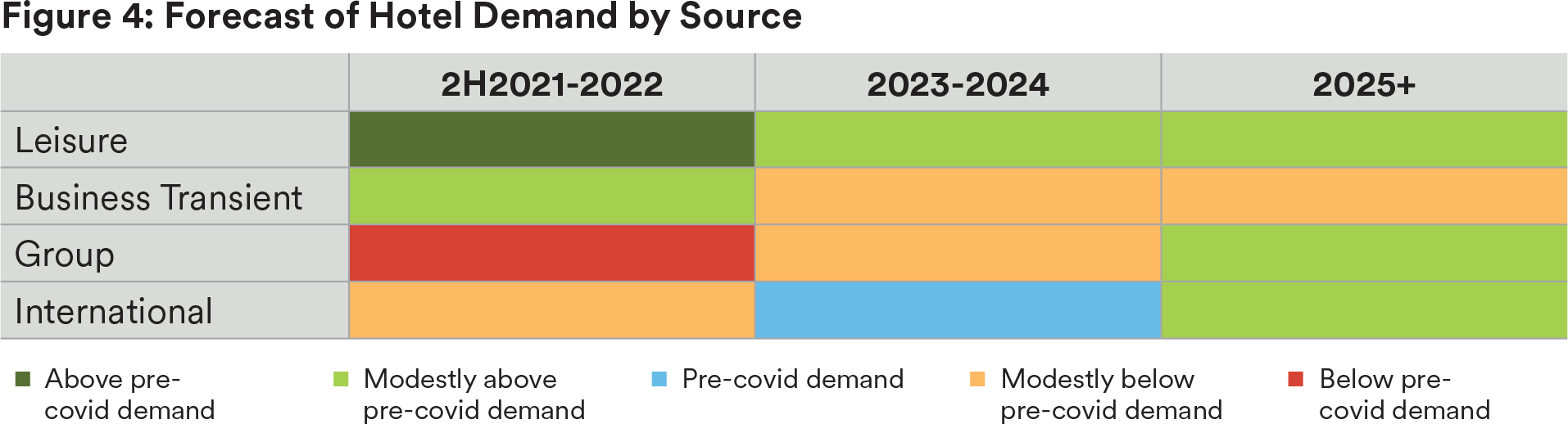

Individuals earning over $70,000 per year have historically been responsible for 75% of hotel spending.4 For this demographic, the recession effectively ended shortly after it began in April of 2020. Job losses have recovered, and employment has now even surpassed pre-COVID levels.5 Personal savings has also increased sharply.6 This is very much different than in prior recessions, such as the Global Financial Crisis, when higher income groups contended with elevated unemployment for several years, and leisure travel was slow to recover. We believe the economic picture alone suggests a surge in leisure travel later in 2021, even before accounting for pent-up demand that surveys suggest has been growing over the last six months. Data from online vacation services support this view, showing a correlation between vaccine distribution and summer 2021 travel bookings.7 Beyond 2022, we believe the secular trend of experienced based spending growth8 will continue to boost leisure travel, and leisure hotel demand will remain in excess of pre-COVID levels.

Our outlook for leisure travel is positive, but post-pandemic business travel may be more challenging to forecast. Although we believe the historical relationship between job growth and RevPAR (cited earlier) is a reasonable starting point in the forecast, there are some additional considerations. Hotels that cater to large group/conference travel may experience a delayed recovery given that social distancing advisories may be in-place through 2022. Group hotels face the additional burden of deriving a larger portion of revenues from food & beverage components, unlike limited-service hotels more commonly associated with transient travel. As such, these assets may not fully recover until 2025.

Hotels that support transient business travel9 may also face challenges in coming years. We estimate that corporate travel budgets will be 25% below pre-covid levels in 2021, and 15% below in 2022. That said, the slowdown in 2021 may have been front loaded, and we expect temporary rebound in transient travel as offices reopen during the second half of 2021. Additionally, a mix of industries from entertainment to biomedical engineering have experienced rapid growth during the pandemic, and certain roles in those sectors could benefit from travel, in our view.

Hotels that support transient business travel9 may also face challenges in coming years. We estimate that corporate travel budgets will be 25% below pre-covid levels in 2021, and 15% below in 2022. That said, the slowdown in 2021 may have been front loaded, and we expect temporary rebound in transient travel as offices reopen during the second half of 2021. Additionally, a mix of industries from entertainment to biomedical engineering have experienced rapid growth during the pandemic, and certain roles in those sectors could benefit from travel, in our view.

Over the medium and longer term, we expect business transient demand to face headwinds from the increased adoption of virtual meetings. Based on a variety of industry surveys conducted pre-and-post COVID, we expect a 15% structural decline in transient business demand.

Lastly, international travel is likely to be slower to recover as many countries have less vaccine access than the U.S., making extended flights less safe. Although this could suggest a slower recovery in markets like New York, Miami, Los Angeles, and San Francisco, increases in domestic leisure travel are already helping to offset it. For example, hotels in Miami experienced occupancy rates nearing 80% during the Martin Luther King holiday weekend in January, similar to pre-COVID levels.10

A Softer Landing

The COVID pandemic has introduced some long-term structural headwinds for hotels, but we believe it has also offered two self-correcting mechanisms that help offset the risk; namely, a reduced supply pipeline and the rise of digital nomads as a new source of hotel demand.

Leading into the COVID crisis, the hotel sector was contending with an elevated supply pipeline, with U.S. hotel stock projected to increase 13.5% between 2020 and 2025. Today, forecasts show the supply pipeline has moderated, and now stands at 9.2% of current stock.11 This figure also does not reflect the likelihood of a portion of hotel stock that may go offline or be converted to an alternative use such as multifamily, further constraining supply. New York, for example, has proposed zoning changes for hotels in order to support housing affordability in the metro.12

In addition to a moderating supply pipeline, COVID-19 has also created a new source of hotel demand in the form of the digital nomad. An acceleration in flexible working arrangements means individuals can work from anywhere and are not consigned to working in their homes. The extended duration of hotel stays during lockdown provides some early evidence of this, and we believe the trend will persist in a post-pandemic world.

Prior to COVID, U.S. employees took on average 17 days off per year and used 8 days for travel. The top 3 reasons for individuals not traveling more during the year all reflected a lack of workplace flexibility.13 We believe newly formalized remote or flex working policies among 10’s of millions of office workers could increase the average number of travel days per year, adding to hotel demand.

Capital Market Conditions

Unlike other real estate sectors, and unlike the broader non-real estate investment universe, we believe the hotel sector is experiencing a capital markets and liquidity crunch. In hotel equity markets, we estimate that prices declined between 10% and 60% depending on the asset characteristics.

Part of the reason our price estimate is so wide relates to varying characteristics of hotel assets, with limited-service hotels generally faring better than full-service hotels. Limited-service hotels have historically had lower volatility NOI changes, and we believe this is largely due to the lower average fixed costs limited-service hotels have compared to full-service hotels. Full-service hotels are also more exposed to group travel, which as we outlined has seen the most severe COVID related demand impact.

A second reason our price decline estimate is so wide relates to the bid-ask spread that persists, and depressed levels of transactions that are occurring. Just $12 billion in hotel properties changed hands in 2020, and nearly half of that occurred in the first quarter (before the Covid recession began). This total is down from an average of $37 billion per year in 2017-2019.14 Transaction volume has grown during the early months of 2021, but is unlikely to recover to pre-covid levels in the near-term, in our view. Current owners of hotels are largely unwilling to accept what they view as discounted offers for their properties in hopes of a significant rebound in business once a greater portion of the population is vaccinated and/or herd immunity is achieved.

Lending activity has also slowed materially. Hotel originations across lender types declined by 79% year-over-year in 2020, a more significant decline than retail (-72%) and office (-56%).15 Although activity has been modestly picking up in 2021, we believe it will also remain well below pre-COVID levels in the near term, similar to equity markets.

In the mortgage investing space, many non-CMBS lenders have been willing to grant payment deferments (but not forgiveness). We believe patience to keep deferring is coming to an end, and we expect subordinate debt and preferred equity opportunities to become more prevalent.

In the CMBS space, we estimate 15% of conduit hotel loans are 90+ days delinquent, or $7.5 billion of principal balance, as of this writing. We believe these borrowers may also contribute to a growing universe of subordinate debt and preferred equity offerings.

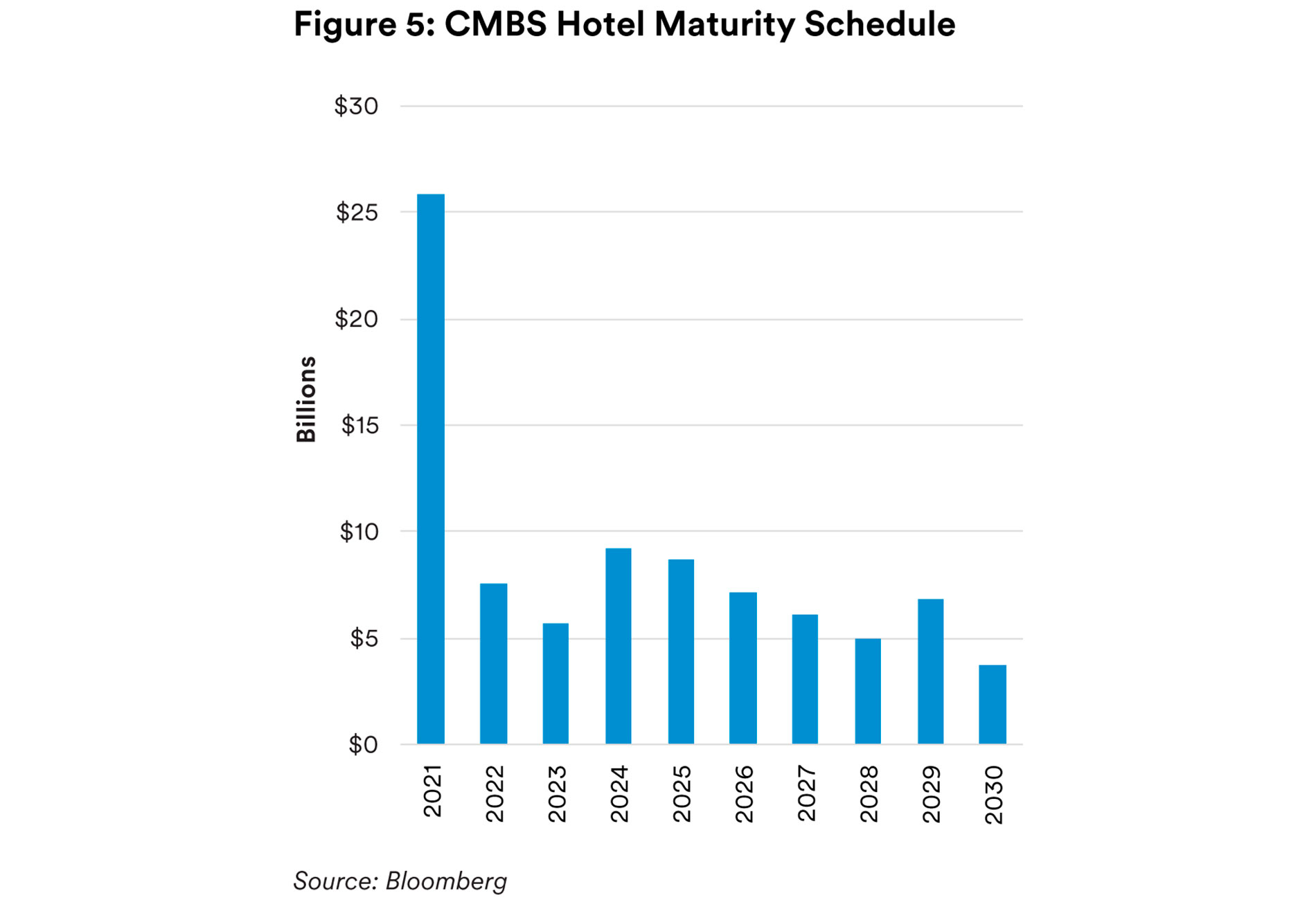

Aside from level of distress in the hotel sector, the CMBS universe also reveals that there is simply a lot of debt that will need to be refinanced over the next several years.

About 30% of outstanding hotel loans in CMBS matures in 202116, though some of that $25 billion set to mature could be pushed into 2022, and to a lesser degree 2023, via extension options. This likely mirrors maturities schedules across other lender types. In addition, we have observed that many hotels that are not facing refinance risks have nonetheless been seeking “rescue” operating capital. Traditional financing sources have been requiring higher coupons, and these sources alone may not be sufficient to support the demand for hotel liquidity during the remainder of 2021 and into 2022. As such, we believe the number of attractive opportunities for investors in the hotel debt space could remain strong in coming quarters.

Conclusion

This past year became the most difficult on record for investors in the hotel sector. Market turbulence, though, often presents opportunities to investors who remain in the market. Today, the hotel sector continues to face challenges, but we believe the most difficult period for hotel demand is behind us. In the very short-term, we believe investors who can provide liquidity to the hotel market could be rewarded with outsized returns.

Endnotes

1 The modeled RevPAR depicted in Exhibit 1 was calculated with a linear regression of office using employment and hotel construction levels to estimate changes in hotel Revenue Per Available Room (RevPAR). The linear regression, or “modeled RevPAR” explained 74.1% of observed RevPAR changes. Data sources included BLS and Moody’s Economy.com for employment growth, STR for hotel construction, and STR for RevPAR changes. Data queried in March 2021.

2 STR. February 2021.

3 Based on current run-rate of 2.2 million vaccine doses per day, with 18% of the U.S. receiving at least one dose, March 10, 2021. Also see: https://www.nytimes.com/live/2021/03/10/world/covid-19-coronavirus#biden-will-announce-he-intends-to-secureanother-100-million-doses-of-johnson-johnsons-vaccine

4 US Census. Data queried in February 2021.

5 Opportunity Insights, as of December 2020, Queried March 2021.

6 St. Louis Fed, as of January 2021, Queried March 2021.

7 https://www.cnbc.com/2021/03/24/is-it-safe-to-travel-this-summer-optimistic-travelers-booking-now-.html

8 See also: The Age of Experienced Based Retail, by MetLife Investment Management.

9 Transient business travel is individuals or small groups administering client support, business development, etc.

10 https://www.hospitalitynet.org/news/4103163.html

11 CBRE-EA, 4Q2020.

12 https://therealdeal.com/2021/01/20/state-proposes-zoning-override-for-commercial-to-resi-conversions/

13 U.S. Travel Association, State of American Vacation. 2018.

14 RCA, February 2021.

15 Mortgage Bankers Association, 4Q2020.

16 Bloomberg. February 2021.

Disclosure

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors.

This document has been prepared by MetLife Investment Management (“MIM”)1 solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results.

In the U.S. this document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor.

This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address Level 34 One Canada Square London E14 5AA United Kingdom. This document is only intended for, and may only be distributed to, investors in the EEA who qualify as a Professional Client as defined under the EEA’s Markets in Financial Instruments Directive, as implemented in the relevant EEA jurisdiction. The investment strategy described herein is intended to be structured as an investment management agreement between MIML (or its affiliates, as the case may be) and a client, although alternative structures more suitable for a particular client can be discussed.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council “GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).&

For investors in Japan - This document is being distributed by MetLife Asset Management Corp. (Japan) (“MAM”), a registered Financial Instruments Business Operator (“FIBO”).

For Investors in Hong Kong - This document is being issued by MetLife Investments Asia Limited (“MIAL”), a part of MIM, and it has not been reviewed by the Securities and Futures Commission of Hong Kong (“SFC”).

For investors in Australia, this information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

1 MetLife Investment Management (“MIM”) is MetLife, Inc.’s institutional management business and the marketing name for subsidiaries of MetLife that provide investment management services to MetLife’s general account, separate accounts and/or unaffiliated/third party investors, including: Metropolitan Life Insurance Company, MetLife Investment Management, LLC, MetLife Investment Management Limited, MetLife Investments Limited, MetLife Investments Asia Limited, MetLife Latin America Asesorias e Inversiones Limitada, MetLife Asset Management Corp. (Japan), and MIM I LLC.

2 As of December 31, 2020. At estimated fair value. Represents the value of all commercial mortgage loans and real estate equity managed by MIM, presented on the basis of gross market value (inclusive of encumbering debt). At estimated fair value. Includes MetLife general account and separate account assets and unaffiliated/third party assets.

Unless otherwise noted, none of the authors of the articles on this page are regulated in Ireland.