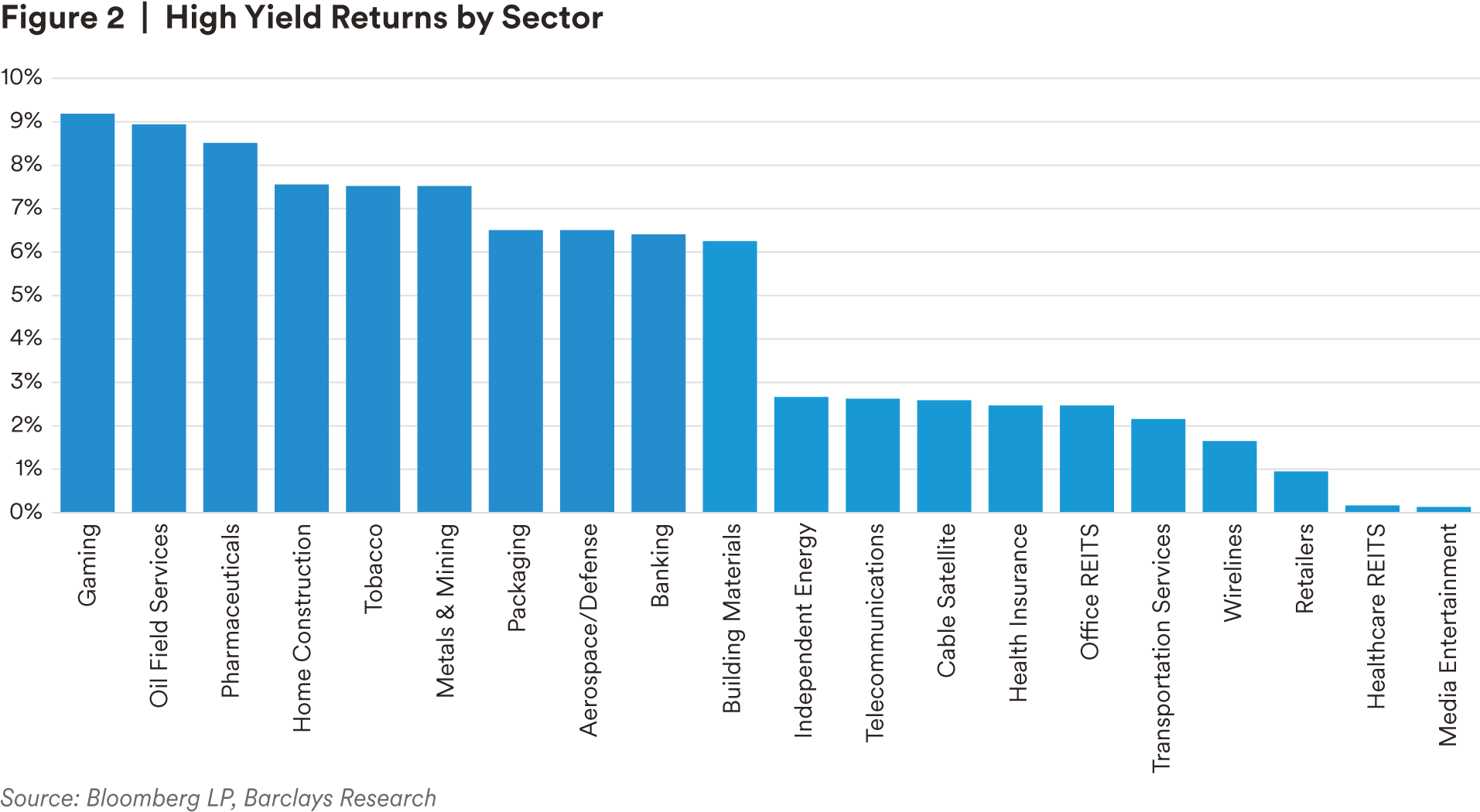

HY bonds closed out the year with October and November posting the strongest two-month rally since 2020. The Bloomberg US HY Index returned 4.17% in the fourth quarter to put 2022 returns at -11.2% after hitting a low of -14.9% at the end of Q31 . Gaming was the top performing sector as China witnessed significant easing of the country’s Zero-COVID policy, supporting Macau gaming issuers within the index2

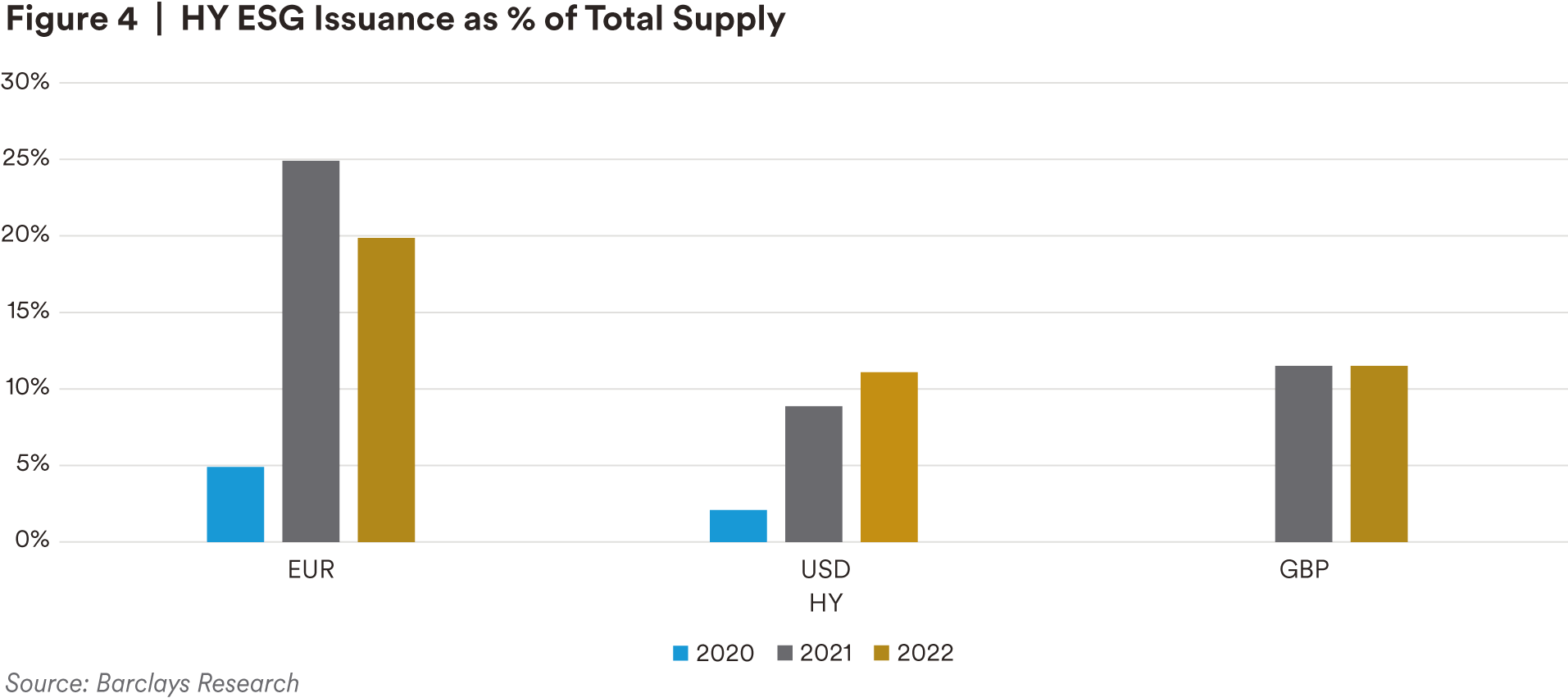

HY bond issuance for 2022 of $102 billion was down over 75% from 2021, as rising yields and market volatility froze primary activity. Q4 issuance of $16.5 billion was the lowest quarter of issuance since Q1 20093 . Although 2022 was a down year for primary activity across credit markets, ESG issuance as a percentage of total corporate supply continued to rise. Notably, green bonds expanded their market share in the labeled issuance space year-over-year, while sustainability-linked bonds make up a smaller proportion of the market than they did last year. Green bond issuance should continue to dominate the labeled market in 2023 as issuers may look to avoid additional interest expense in an elevated rate environment.

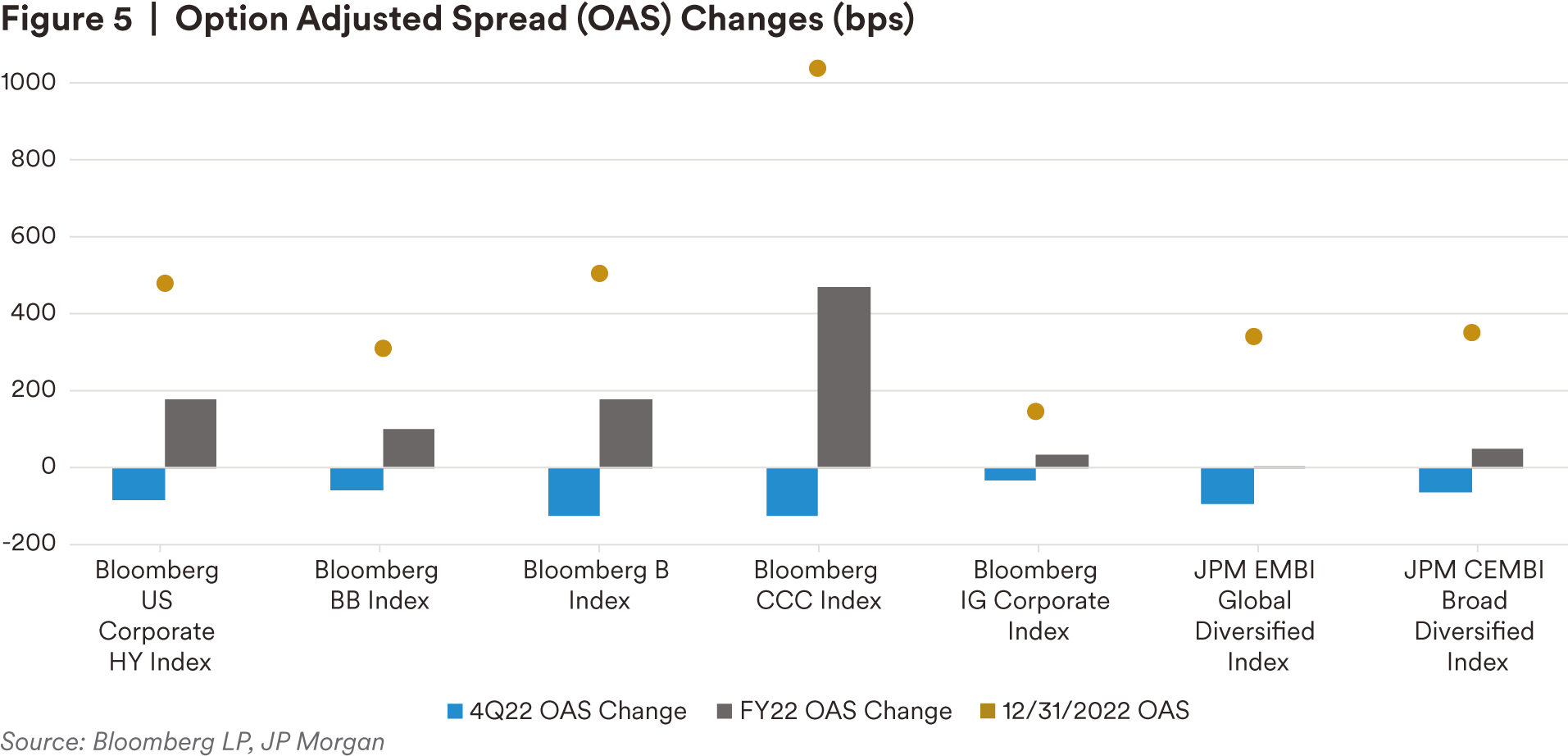

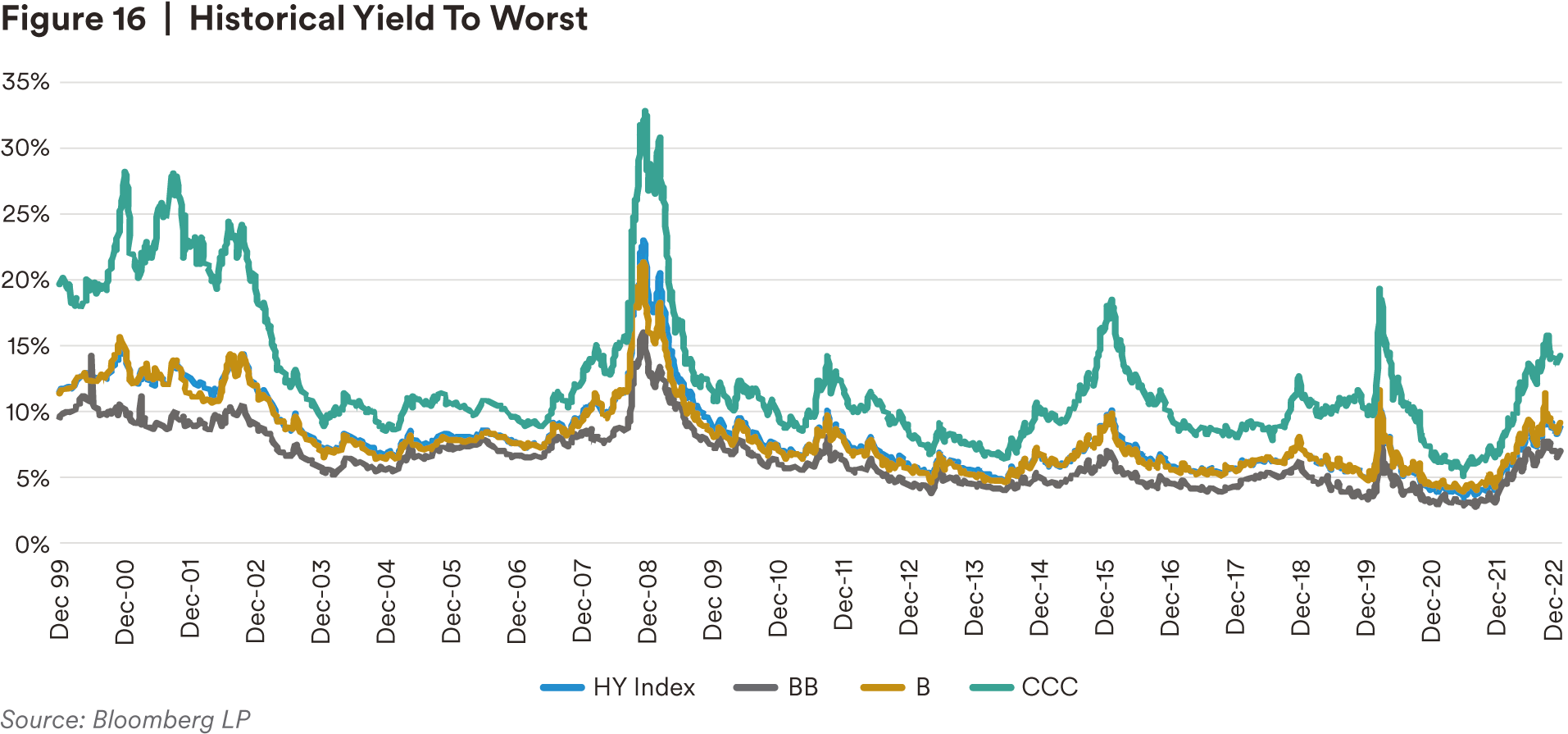

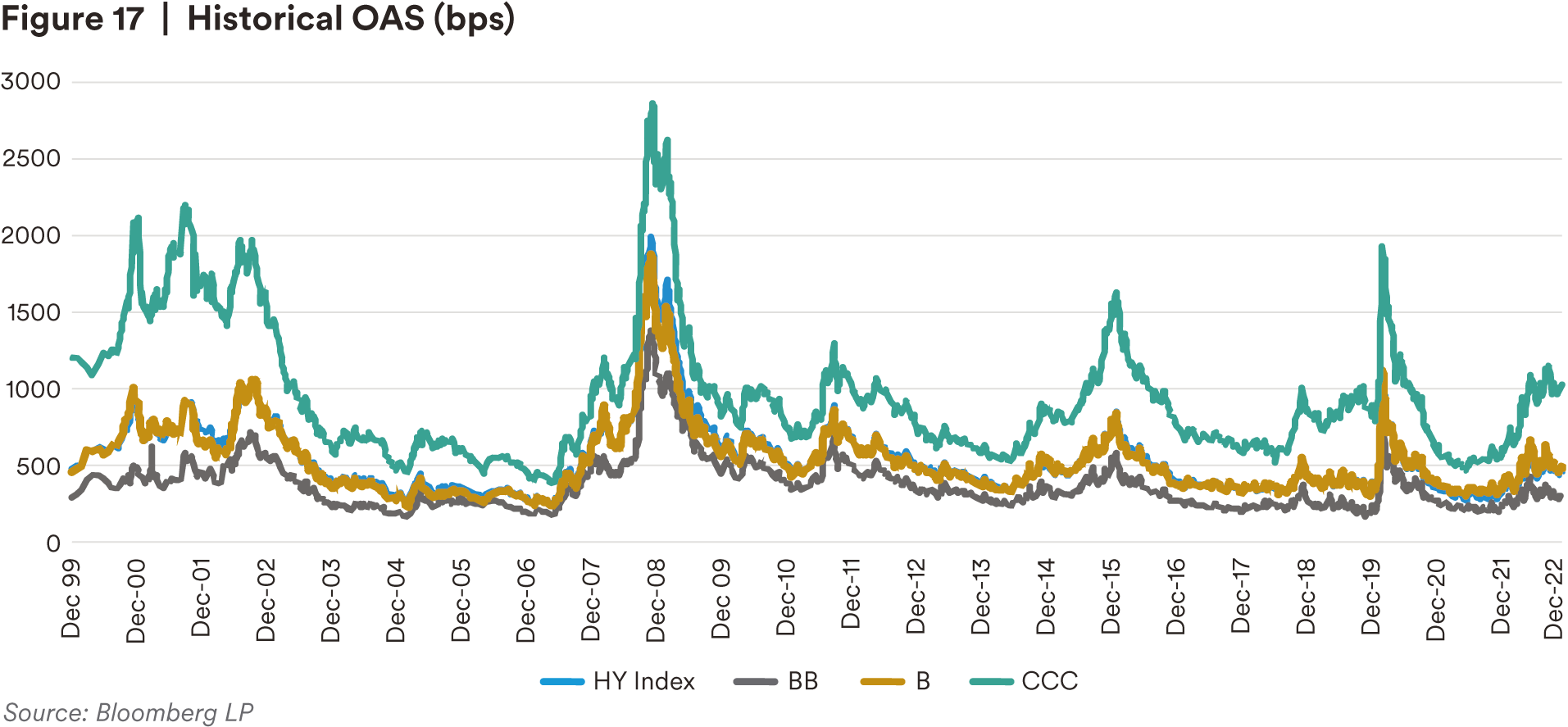

In Q4, spreads tightened across all credit quality with single-B credit experiencing the most tightening in the quarter. However, for the year, spreads widened 101bps for BBs, 176bps for Bs, and 459bps for CCCs. The increase in yield was even more dramatic with yields increasing almost 400bps for BBs, 464bps for Bs, and 744bps for CCCs4. The increase in yield was even more dramatic with yields increasing almost 400bps for BBs, 464bps for Bs, and 744bps for CCCs . Given the combination of wider spreads and higher Treasury yields, yields across High Yield ended the year cheap to their 20yr long-term average.

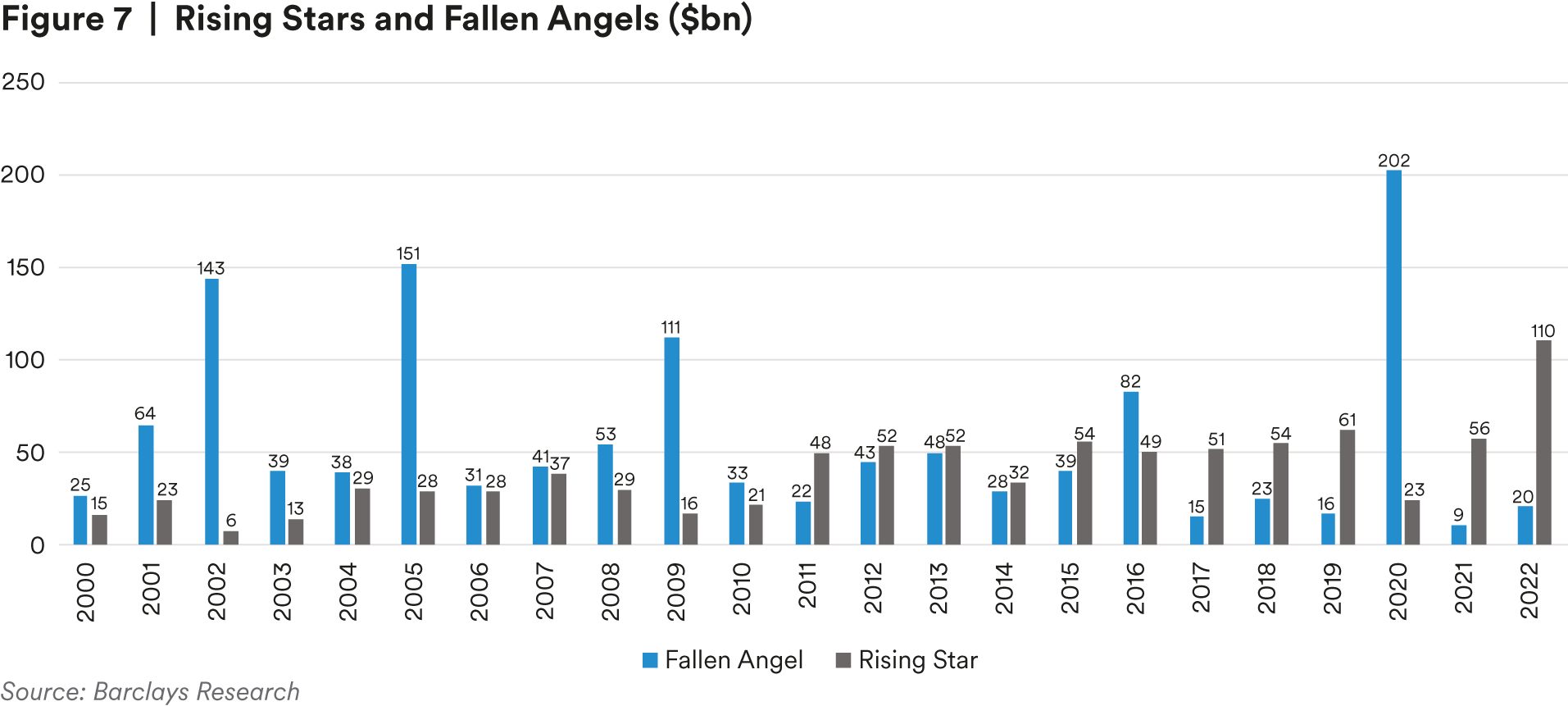

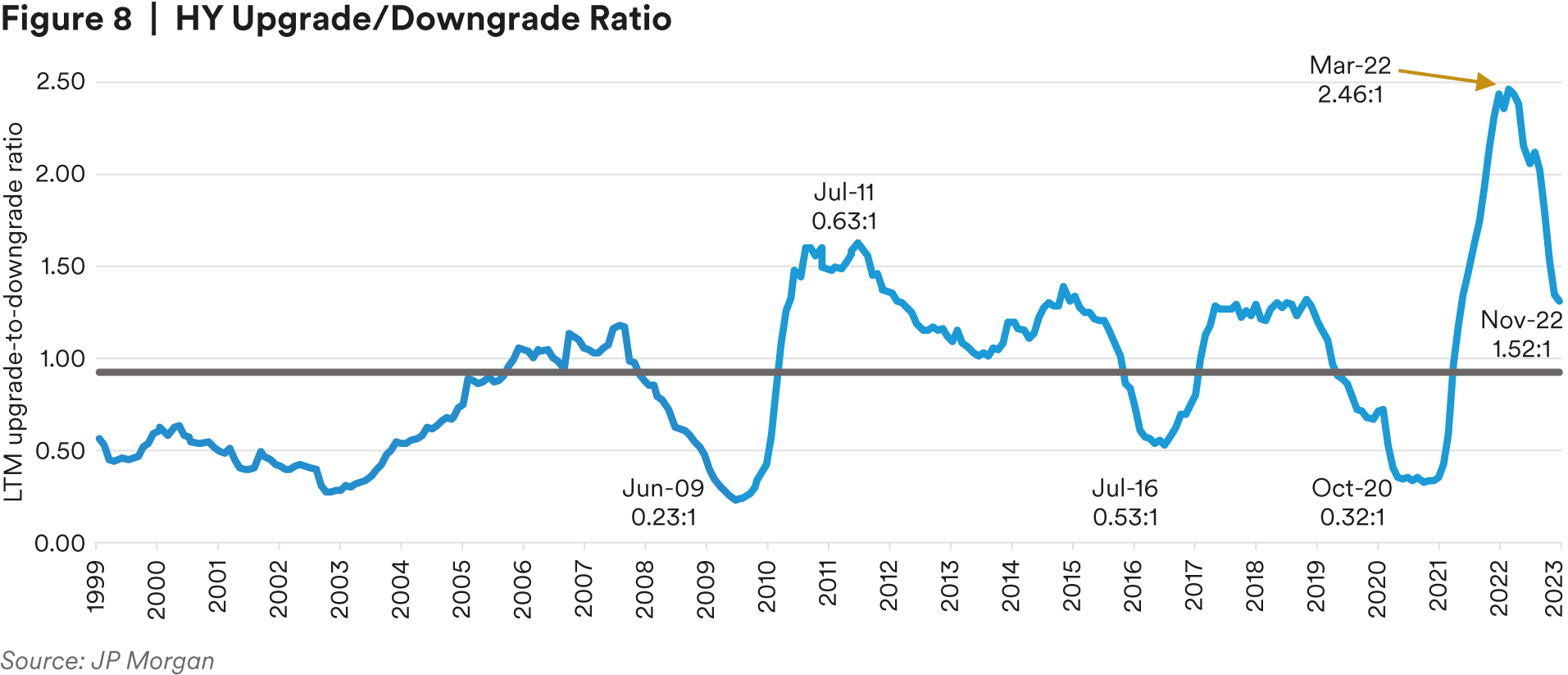

Fallen angels remain at extremely low levels while the index recorded a record amount of rising stars as companies focused on improving credit metrics. Despite this, we have seen an uptick in downgrades, as the upgrade/downgrade ratio has peaked and is projected to decline as the cycle progresses.

Outlook:

We maintain a cautious risk appetite heading into 2023 as spreads remain tight amid an uncertain macroeconomic environment, where there is potential for further spread widening. Uncertainty around economic data continues, and Q4 earnings reports will prove critical; however, as the possibility of a soft-landing recession gains increased traction, there is opportunity for high yield to outperform. With spreads almost 100 basis points through long term averages, valuations do not appropriately reflect the current macro headwinds. Yet this more challenging fundamental backdrop will likely translate into increased sectoral dispersion, ratings decompression, and wider spreads in 2023, opening the door to opportunities within HY. Following a historically low year of issuance in the high yield primary market, we expect issuance to modestly rebound in the new year, providing opportunities to capitalize on new issue concessions as investors begin seeking market access once again.

Despite concerns of a recession on the horizon, the HY market has data indicating that issuers are better prepared than historically to weather the storm. As such, we remain comfortable with issuers’ abilities to continue servicing debt even in the face of challenging macro headwinds. While we feel corporate fundamentals remain strong, we do expect a lag in tighter financial conditions to weigh on high yield credits in 2023 and are positioned accordingly, with security selection remaining essential.

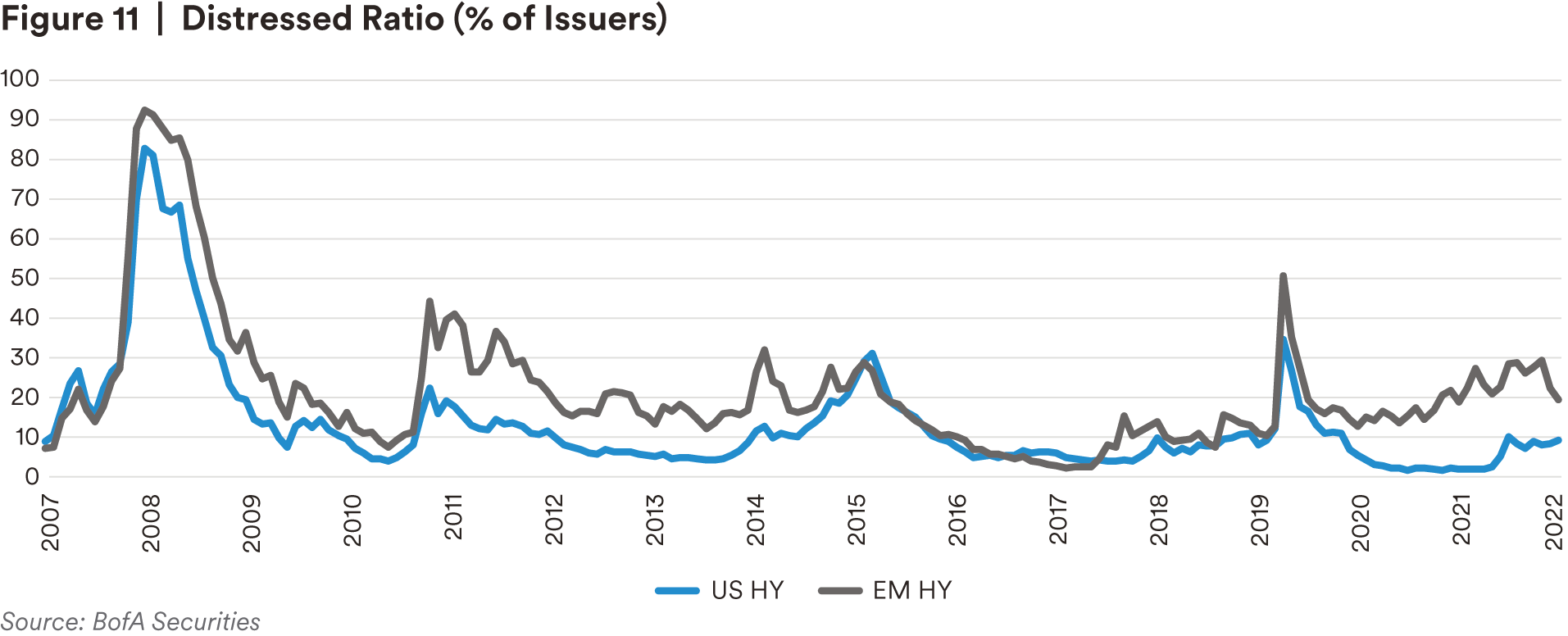

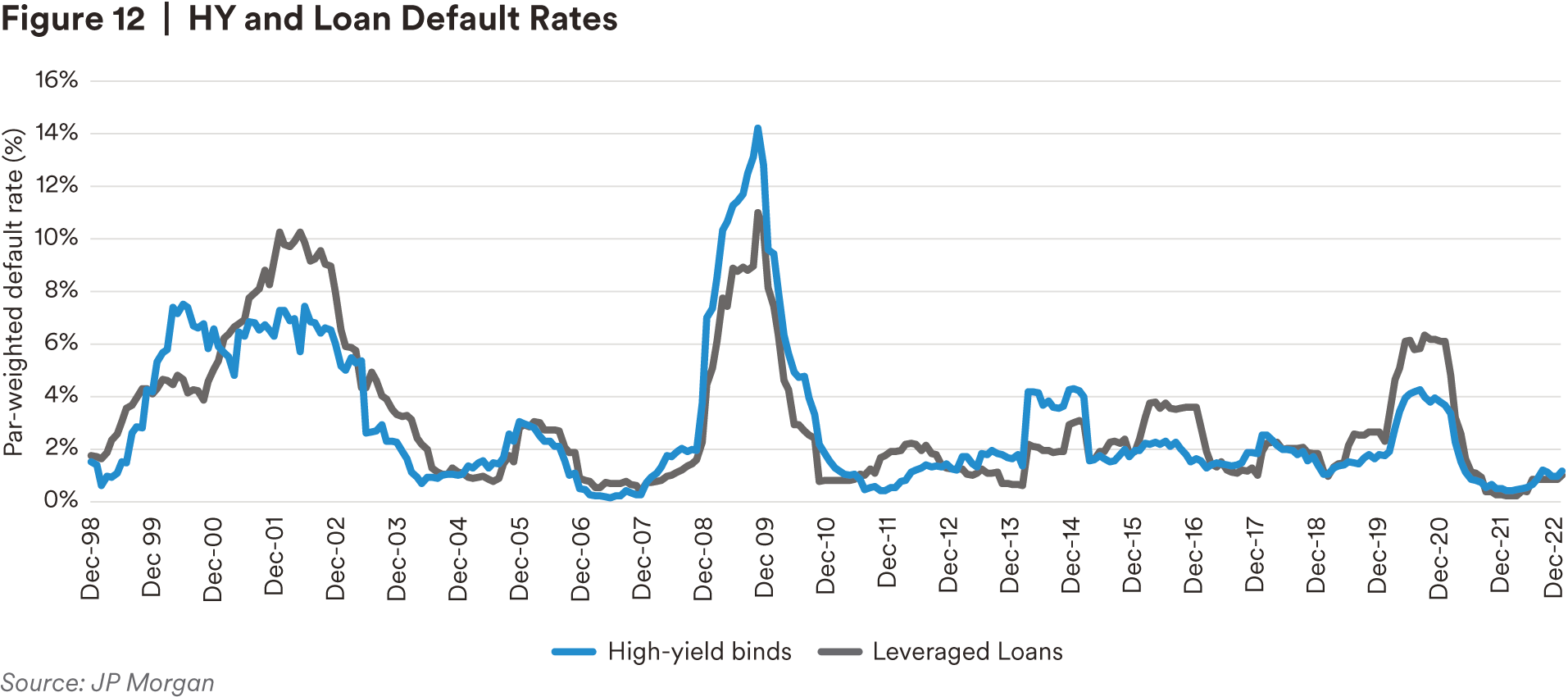

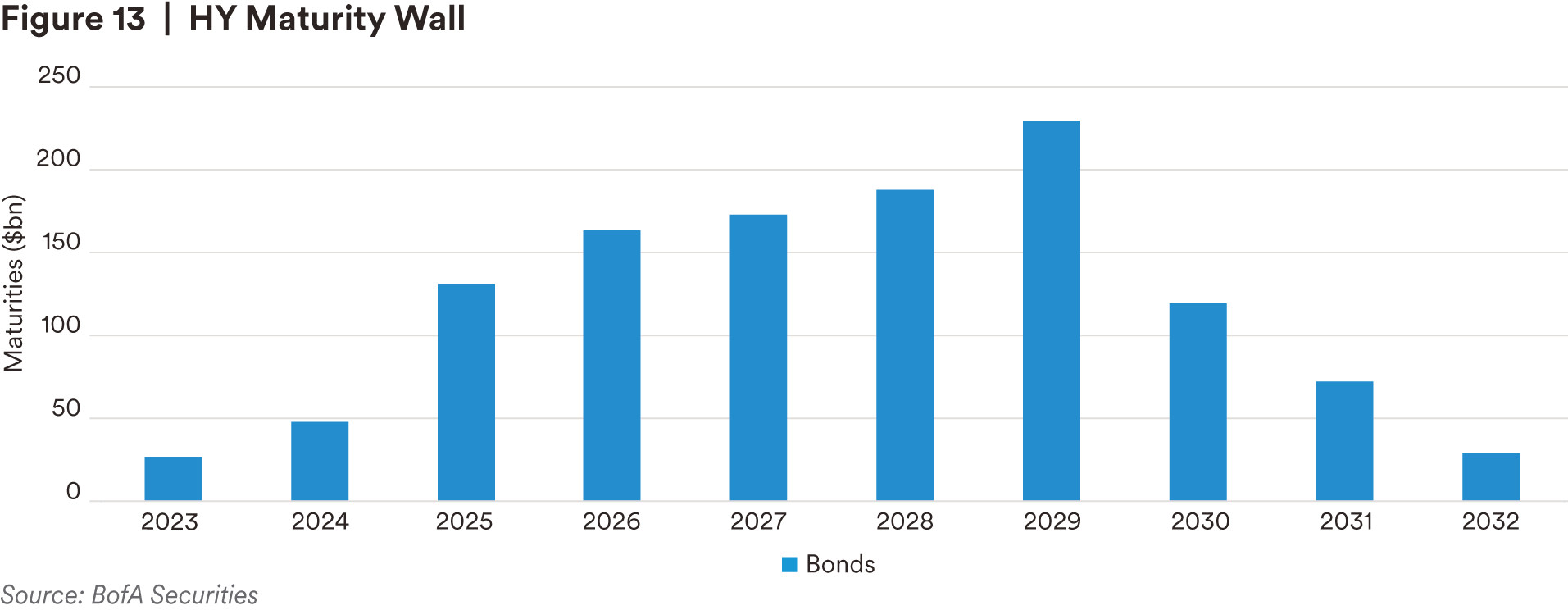

While we do expect to see an uptick in defaults as recession risk increases, the current distressed ratio remains below 10% of US HY issuers. In addition to supportive fundamentals, manageable near-term maturities should help keep the default rate below traditional recessionary periods. We believe the maturity wall for 2023 and 2024 is manageable, providing flexibility for issuers to weather the near-term outlook.

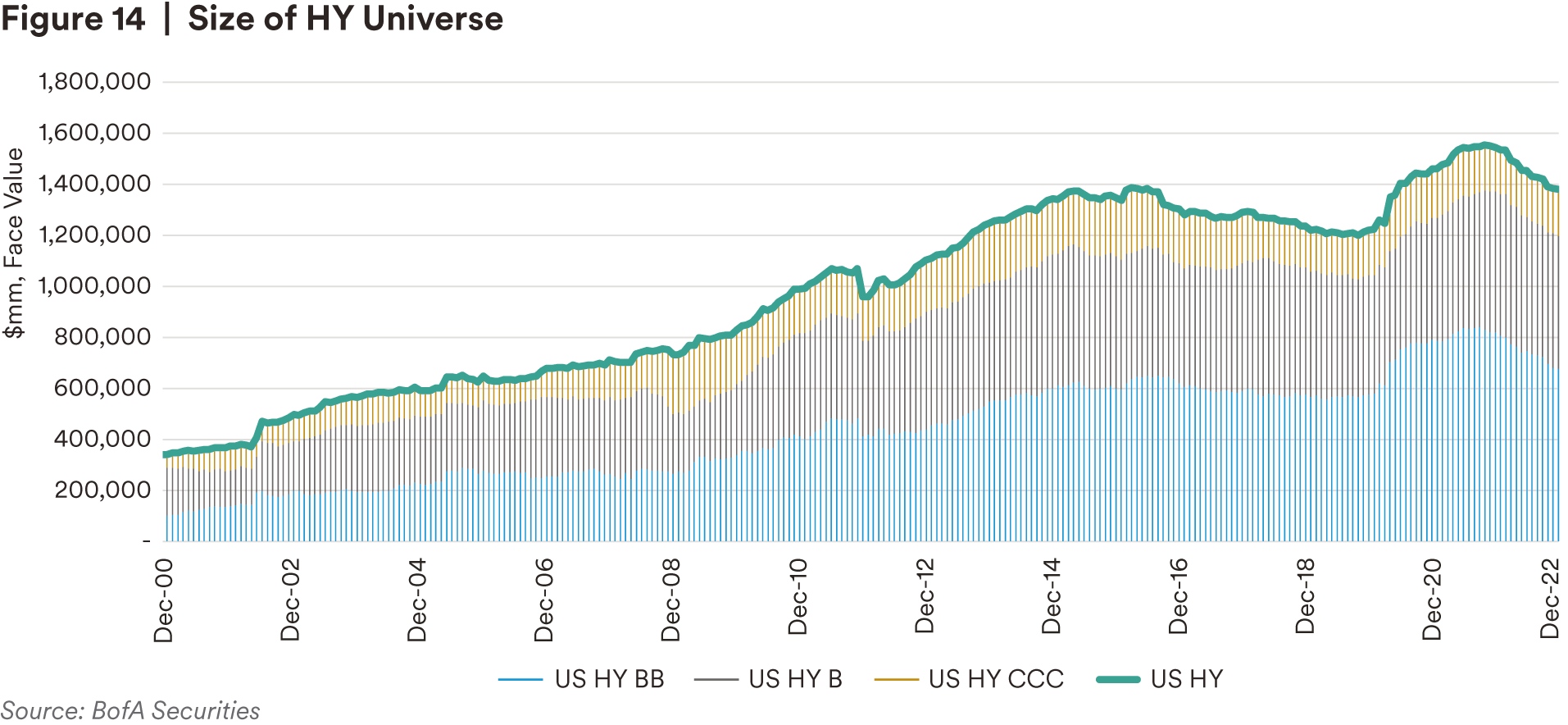

Given the lack of new issuance in the HY market as investors turn to alternative funding sources as maturities come due, the size of the market has been decreasing. Riskier issuers such as LBOs have utilized the bank loan and private credit markets opportunistically over the last few years. As a result, the HY market has not taken on those additional risks as it has in other sustained market rallies. Additionally, lower quality investors have been shut out of the market due to volatility and higher costs of funding. As a result, the overall credit quality of the market has gone up, with the CCC space decreasing. We believe this additional technical will continue to support a lower default rate in the face of a recession.

From an absolute yield perspective, the HY market looks enticing with the current index level near 9%. We believe even within the high-quality space, which is well positioned in a recession scenario, a yield above 7% provides attractive opportunities to investors.

Endnotes

1 Bloomberg LP

2 Barclays Research

3 Barclays Research

4 Bloomberg LP

Disclosures

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors. This document has been prepared by MetLife Investment Management (“MIM”)1 solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results.

In the U.S. this document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor.

This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address 1 Angel Lane, 8th Floor, London, EC4R 3AB, United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK and EEA who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as implemented in the relevant EEA jurisdiction, and the retained EU law version of the same in the UK.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Asset Management Corp. (Japan) (“MAM”), 1-3 Kioicho, Chiyoda-ku, Tokyo 102-0094, Tokyo Garden Terrace KioiCho Kioi Tower 25F, a registered Financial Instruments Business Operator (“FIBO”) under the registration entry Director General of the Kanto Local Finance Bureau (FIBO) No. 2414.

For Investors in Hong Kong S.A.R.: This document is being issued by MetLife Investments Asia Limited (“MIAL”), a part of MIM, and it has not been reviewed by the Securities and Futures Commission of Hong Kong (“SFC”). MIAL is licensed by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

MIMEL: For investors in the EEA, this document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. Unless otherwise stated, none of the authors of this article are regulated in Ireland.

1 MetLife Investment Management (“MIM”) is MetLife, Inc.’s institutional management business and the marketing name for subsidiaries of MetLife that provide investment management services to MetLife’s general account, separate accounts and/or unaffiliated/third party investors, including: Metropolitan Life Insurance Company, MetLife Investment Management, LLC, MetLife Investment Management Limited, MetLife Investments Limited, MetLife Investments Asia Limited, MetLife Latin America Asesorias e Inversio