The “Music” May Stop in Late 2023

Taming inflation is the main theme for global economies. Tightening monetary policy, slower growth and rising recession risk are all likely having an impact. U.S. — A recession in 2023 remains as our base case (Figure 2) with inflation falling to less than 3% and the unemployment rate rising above 4.5%. Europe — Eurozone economies are expecting weaker growth amid continued contractionary policies as policymakers manage sticky core inflation. Energy issues seem to have abated somewhat, with higher gas reserves than last year. Asia — Growth momentum remains decent for the region, with headwinds likely to build up later in the year. Tighter monetary policy is expected due to the hawkish influence of the Fed and stickier-than-expected inflation. Latin America — Like other economies, GDP growth is likely to decelerate in 2023 due to tighter monetary policies and political uncertainties. Inflation is expected to ease gradually, thanks to a moderation in commodity prices.

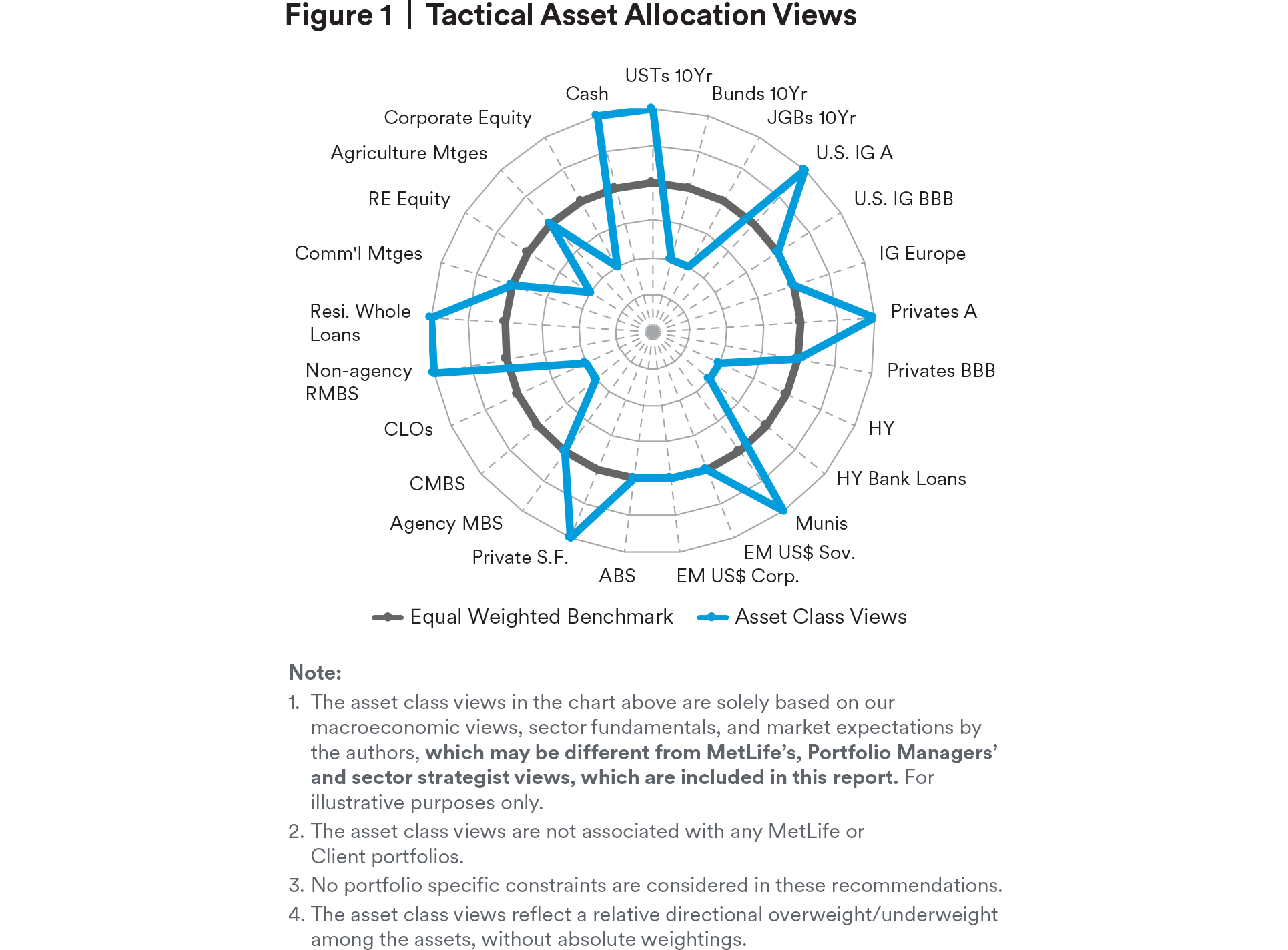

The End of Tightening Cycle May Be Near

U.S. Treasury — We continue to expect the Fed to conclude this hiking cycle by mid-2023 given our view of slowing economic growth and rising recession risk. Bunds — Less generous monetary policy support has seen bund yields rise sharply over the past year but demands for bunds are expected to remain solid, especially during periods of heightened uncertainty. JGBs — The BoJ is likely to prefer to act cautiously rather than tighten prematurely given the risk of returning the economy back to a disinflationary path. We expect the BoJ to continue its JGB purchases, capping the 10yr segment of the curve at around 50bps. CGBs — We expect China rates to remain rangebound in 1Q23 before rising gradually in 2Q23 as the growth recovery gains stronger traction.

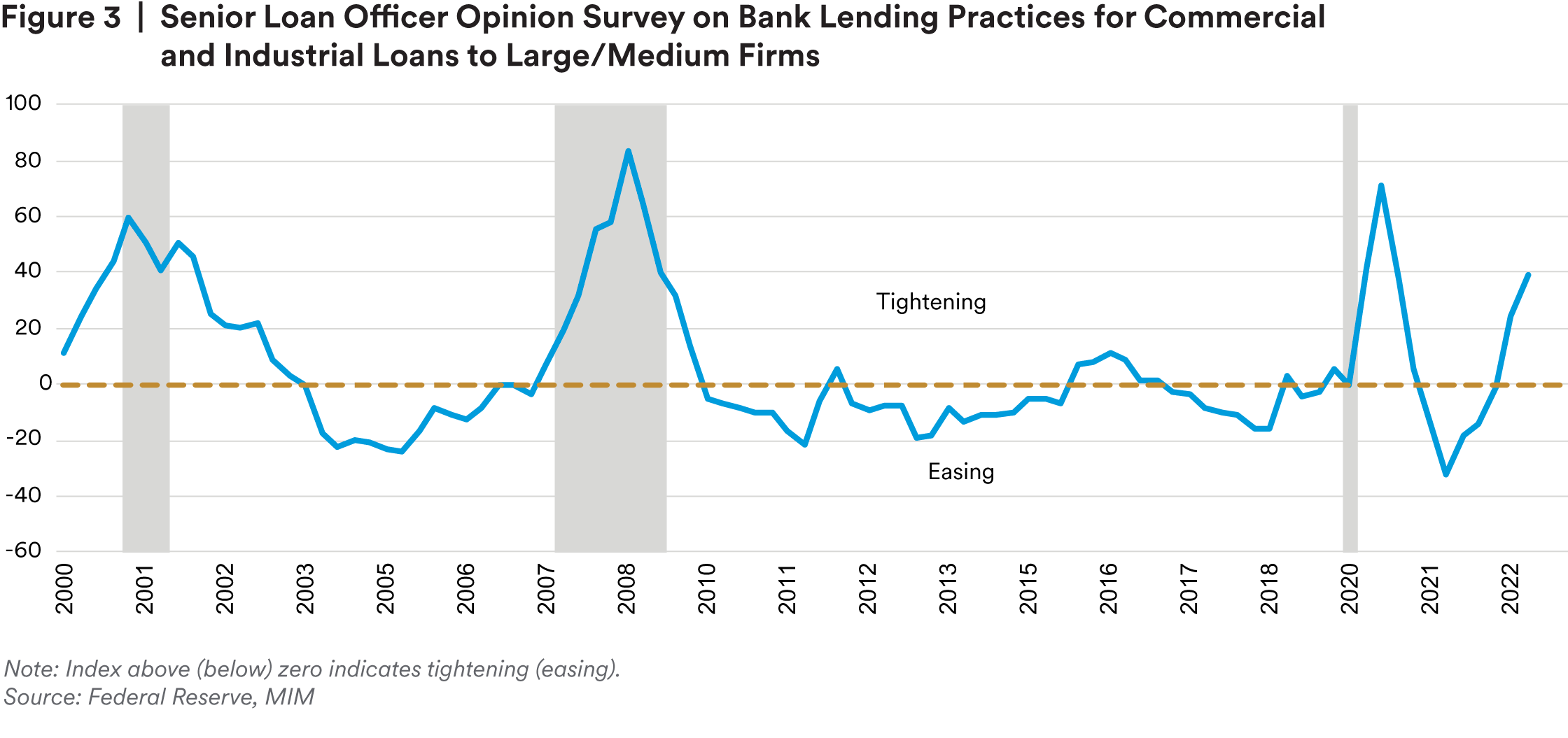

Lending Standards Are Tightening

After a strong start in 2023, the credit market gave back some of the gains since February as the labor market remains tight and inflation remains sticky. Bank lending standards tightened further in 1Q 2023, and banks expected further tightening and credit deterioration in 2023 (Figure 3). We believe that the credit cycle could turn in the next couple of quarters. At the same time, we do not think credit markets have priced in sufficient downside risk just yet. Across credit markets, valuations are still near their historic averages and priced like mid-cycle. Recent banking sector issues have heightened market uncertainty as participants wonder if, after more than a decade of ultra-easing global monetary policies, there could be more volatility as the consequence of one of the most aggressive Federal Reserve hiking cycles in history. Looking forward, we expect spreads to trend wider on heightened recession risk in 2023. As the Fed’s hiking cycle appears to be close to an end, investors may take the advantage of temporary market strength to upgrade portfolio quality. As a result of this expectation, we continue to recommend “up in quality” for 2023. U.S. Investment Grade (IG) — Credit fundamentals showed early signs of weakening in 4Q 2022 as credit metrics deteriorated for the first time since the pandemic. The outlook remains neutral on the prospect of further slowing in profits and margin pressures. While overall EBITDA margins are marginally off cycle highs, ex-energy EBITDA margins have already peaked. The overall leverage ratio has ticked up while the coverage ratio has ticked down in 4Q 2022. IG yields remain near the highest levels since 2009 and we believe current yield levels are attractive.

European IG — Credit fundamentals improved in 4Q 2022. EBITDA growth and margins remain at record highs driven by Energy sector. Ex-Energy margins may continue to be under pressure particularly if inflation remains sticky. ECB slowed down its pace of rate hikes on peaking inflation and confidence recovered on fading energy price shock. In addition, China’s reopening may help offset sluggish regional growth. As a result, we upgraded European IG to neutral from underweight. High Yield — Similar to the IG market (credit fundamentals showed early signs of weakening), while the leverage ratio held steady in 4Q 2022, coverage ratio ticked lower as interest expense outpaced EBITDA growth. Although still benign, defaults picked up in 2022 and continued into 2023. The default rate is expected to rise significantly in 2023. Moody’s expects U.S. default is likely to rise to 5.4% by February 2024 from only 2.5% in February 2023. The bond recovery rate remains above its 5-year average. Leveraged Loans — Due to the prevalence of loan-only capital structures, recovery rates are meaningfully lower than historical averages. Although recovery rate for first-lien loans is still above its 5-year average in February 2023, recovery rates for loan-only issuers over the past 12 months are significantly below those for cross issuers. According to JP Morgan’s Default Monitor, the ratings migration trend has been negative as downgrades outnumbered upgrades again in February for 10 consecutive months. Spreads appear cheap, but we are concerned about higher defaults with lower recovery rates and heightened downgrade risk for leveraged loans in 2023 as the credit cycle turns. Municipals — Both general obligation (GO) and revenue bond outlooks remain sound on a challenging macro outlook. For GOs, total state and local government tax revenue declined 1.0% YoY in 3Q 2022 indicated by Urban Institute’s State Tax and Economic Review, the first decline in this cycle. Coincident indexes weakened further in 4Q 2022 while budget reserves for FY2022 came in higher than expectations and FY2023 are revised higher. For revenue bonds, in healthcare sector, the Omicron surge had a more severe financial impact on not-for-profit (NFP) Hospitals starting in 4Q 2021 and continuing into 2022. While EBITDA margins rebounded sequentially in 2Q 2022 and continued to improve in 3Q 2022 and 4Q 2022, hospitals have to improve productivity, cut costs or increase revenue.

European IG — Credit fundamentals improved in 4Q 2022. EBITDA growth and margins remain at record highs driven by Energy sector. Ex-Energy margins may continue to be under pressure particularly if inflation remains sticky. ECB slowed down its pace of rate hikes on peaking inflation and confidence recovered on fading energy price shock. In addition, China’s reopening may help offset sluggish regional growth. As a result, we upgraded European IG to neutral from underweight. High Yield — Similar to the IG market (credit fundamentals showed early signs of weakening), while the leverage ratio held steady in 4Q 2022, coverage ratio ticked lower as interest expense outpaced EBITDA growth. Although still benign, defaults picked up in 2022 and continued into 2023. The default rate is expected to rise significantly in 2023. Moody’s expects U.S. default is likely to rise to 5.4% by February 2024 from only 2.5% in February 2023. The bond recovery rate remains above its 5-year average. Leveraged Loans — Due to the prevalence of loan-only capital structures, recovery rates are meaningfully lower than historical averages. Although recovery rate for first-lien loans is still above its 5-year average in February 2023, recovery rates for loan-only issuers over the past 12 months are significantly below those for cross issuers. According to JP Morgan’s Default Monitor, the ratings migration trend has been negative as downgrades outnumbered upgrades again in February for 10 consecutive months. Spreads appear cheap, but we are concerned about higher defaults with lower recovery rates and heightened downgrade risk for leveraged loans in 2023 as the credit cycle turns. Municipals — Both general obligation (GO) and revenue bond outlooks remain sound on a challenging macro outlook. For GOs, total state and local government tax revenue declined 1.0% YoY in 3Q 2022 indicated by Urban Institute’s State Tax and Economic Review, the first decline in this cycle. Coincident indexes weakened further in 4Q 2022 while budget reserves for FY2022 came in higher than expectations and FY2023 are revised higher. For revenue bonds, in healthcare sector, the Omicron surge had a more severe financial impact on not-for-profit (NFP) Hospitals starting in 4Q 2021 and continuing into 2022. While EBITDA margins rebounded sequentially in 2Q 2022 and continued to improve in 3Q 2022 and 4Q 2022, hospitals have to improve productivity, cut costs or increase revenue.

Air traffic continues to recover from the 2020 lows. Toll road revenues have largely recovered to pre- pandemic levels. We believe the taxable municipals market is likely to be relatively more resilient in a challenging macro environment. Emerging Market (EM) IG — We expect EM growth to pick up in 2023. LatAm and EMEA growth are still negatively impacted by the lagged impact of monetary tightening and high inflation. Asia appears likely to outperform driven by China’s faster than expected reopening. In China, since the reopening in late 2022, both manufacturing and non-manufacturing PMIs rebounded strongly in 2023 as both measures are already firmly in expansion territory. For EM corporates, outlook remains neutral as quarterly revenues and EBITDA were flat sequentially in 4Q 2022. EBITDA margins are still near cycle peak, and we expect margins to remain healthy but are likely to compress on higher cost pressures. Leverage ratio ticked up in 4Q 2022 as LTM EBITDA deteriorated marginally while debt levels were stable.

Weakest Consumers Are a Concern

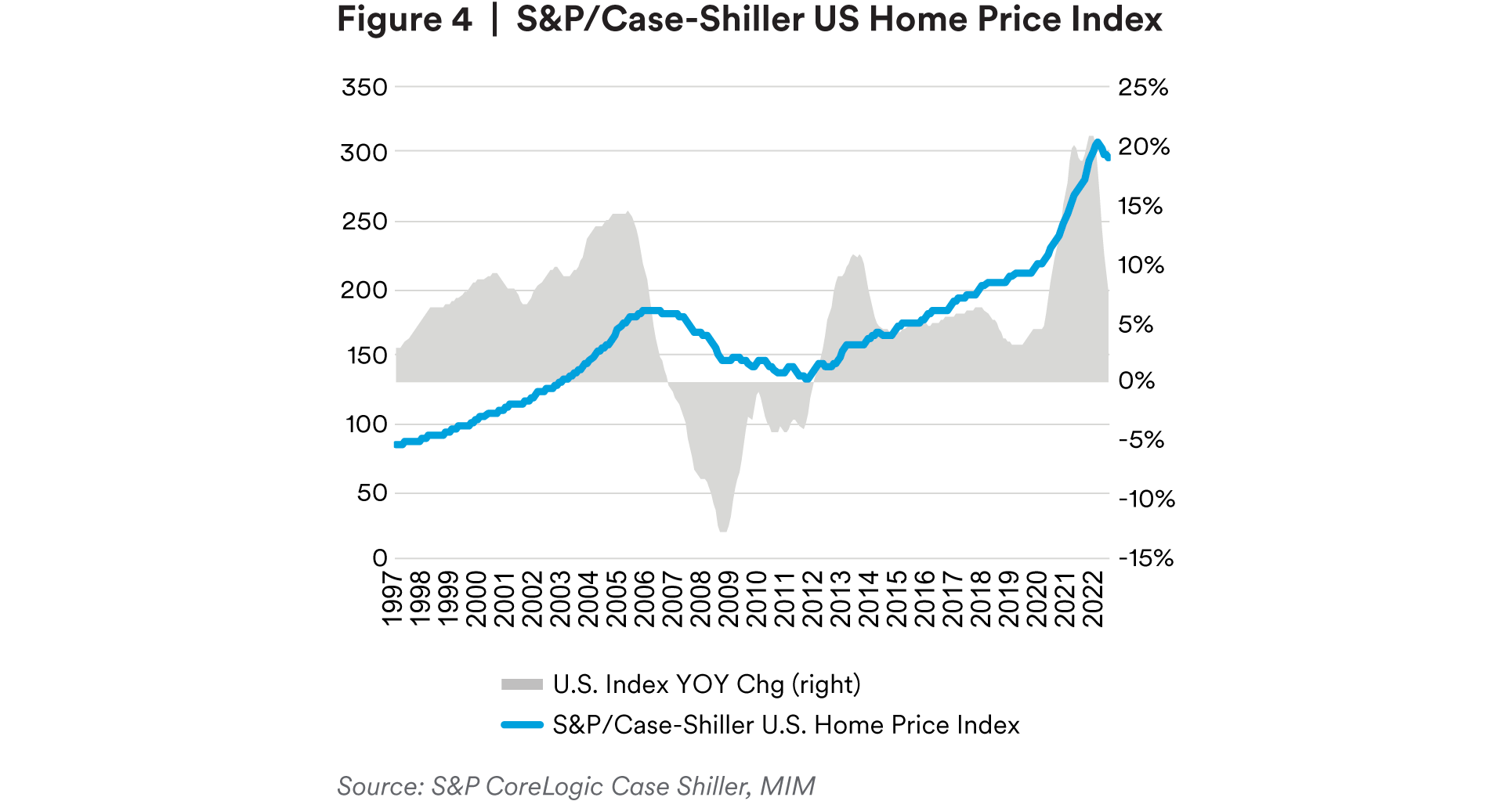

Consumers performance is weaker; Commercial Real Estate lending has contracted; defaults are increasing across all sectors; auto and consumer loan performance deterioration are notable. Weakest consumers are a concern, who have low saving rate, high card balances, high borrowing rate. Residential Credit — Case Shiller 20 City composite down to 6.8% YoY (Figure 4). Mortgage volume is low as few people want to move/buy homes. Spring selling season needs to be watched for housing turnover as well as transaction clarity. Overbuilding is not a concern as the builders are reducing starts significantly to work out existing housing stock. Consumers are also not listing homes for sale reducing supply. Home Equity loans are growing as consumers find ways to access cash without refinancing.

Asset-backed securities (ABS) — The consumer is finally developing some caution as Bureau of Economic Analysis’ Personal Saving rate modestly increased to 3.4% of disposable income while Fed Reserve measures of household debt payments keep increasing. Surprisingly, Conference Board’s consumer confidence index (107.1) and University of Michigan’s consumer sentiment index (66.4) measures are both off their 2022 lows while Manheim Auctions’ auto index (234) surprised to the upside. Lenders continue to tighten standards, reduced card balance limits, and increased yields on borrowing rates. CLO — Issuance recovering as managers look to price deals while volatility has been subdued and markets are open for business. Fundamentals continue to deteriorate with elevated focus on Bank Loan downgrades and corresponding impact on transactions. Failure of over-collateralization ratios infrequent but expected to increase and defaults take hold 2023/2024. CMBS — A precipitous retreat in the lending environment is leading to borrower stress. Percent of loans moving to watchlist/special servicer increasing. Office sector receiving many headlines with several high-profile borrowers reassessing property support. We expect many sponsors to utilize or seek extensions and they may be unable to decrease fixed expenses (taxes) easily. Rating agencies are expected to become more active with downgrade watches leading to poor liquidity and higher cost of funds. Agency MBS — Mortgage origination continues to decline with both the refi and purchase index resting at 20yr lows. Housing turnover is expected to be the main driver of prepayments as 72% of borrowers have mortgage rates of 4% or lower suggested by Goldman Sachs. Current coupon MBS spreads remain wide of historical averages. While valuations are attractive with most asset managers overweight relative to the index, the lack of bank demand continues to weigh on spreads. Private Structured Credit — A very active pipeline is expected in Q2 2023 with healthy sector diversity including consumer, commercial and residential credit. Based on our active pipeline, pricing has generally moved tighter from 300+bps in 4Q22 to the low-mid 200s range driven by the strong rally in public ABS markets. However, in late February ABS spreads broke the tightening trend and finally moved a bit wider. This may alleviate spread compression in the near term.

Real Estate Equity Has Re-priced

Real estate fundamentals remain mostly healthy. We expect that inflation is beginning to cool. Shelter costs which account for nearly a third of the CPI are moving more convincingly toward the Federal Reserve’s target for long-term price growth. While real estate fundamentals for most property types have been stable, capital market conditions have continued to deteriorate, and real estate equity has re-priced.

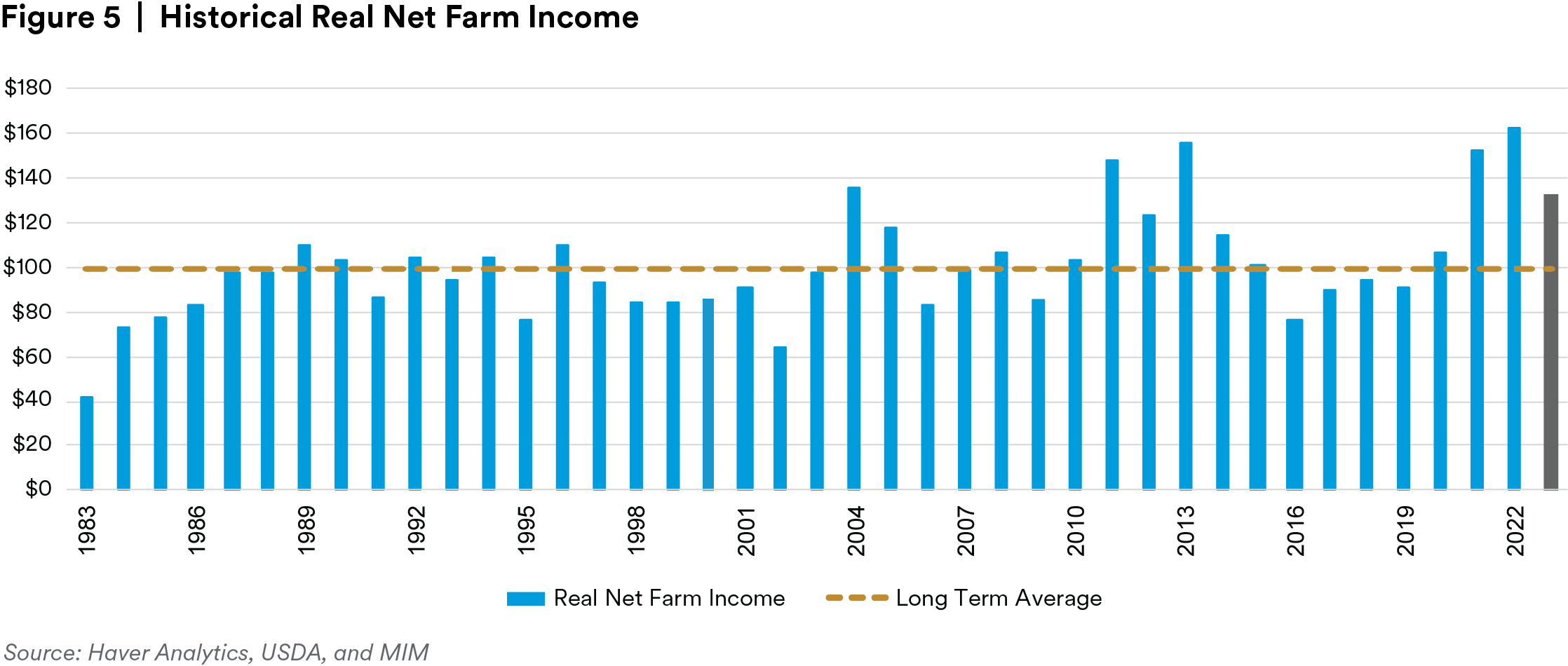

Agricultural Credit Fundamentals Remain Healthy Amid Macroeconomic Volatility

Net farm income will likely decline year-over-year in 2023 after reaching a record level in 2022. Still, easing input costs and elevated commodity prices are expected to keep farm sector profitability above the long-term average this year (Figure 5). Exports of corn and soybean — key agricultural products that drive farm incomes — have declined but remain near the ten-year average. Drought conditions in South America and low global inventories are anticipated to support agricultural commodity prices and producer incomes in 2023. According to American Bankers Association, farm real-estate loan demand in 2022 grew nearly 10%, and average delinquency rates remained at all-time lows. Above-average profitability and strong asset values will likely continue to support farm lending activity this year. Though, the recent stress in the overall banking system could result in a lending pullback from some regional banks and reduce competition on select transactions. Agricultural mortgage spreads could also be impacted by any additional rate hikes in 2023.

Safe Haven Assets Are Preferred Over Risky Assets

Given our view of recession in 2023 and the continued yield curve inversion, cash looks like a safe haven that may generate a better risk-adjusted return in the short run. US 3-month Treasury bills, for example, reached as high as 4.9% in March 2023 indicated by Bloomberg, the highest level since 2007. With the possibility of further rate hikes and banking system stresses continuing into the second quarter, public equities are expected to remain volatile. As a result, we continue to hold our risk-off view and prefer safe haven assets as positioning ahead of an expected pending recession.

Disclaimer

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors.

This document has been prepared by MetLife Investment Management (“MIM”)1 solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results.

In the U.S. this document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor.

This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address 1 Angel Lane, 8th Floor, London, EC4R 3AB, United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK and EEA who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as implemented in the relevant EEA jurisdiction, and the retained EU law version of the same in the UK.

MIMEL: For investors in the EEA, this document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such)

For investors in Japan: This document is being distributed by MetLife Asset Management Corp. (Japan) (“MAM”), 1-3 Kioicho, Chiyoda-ku, Tokyo 102- 0094, Tokyo Garden Terrace KioiCho Kioi Tower 25F, a registered Financial Instruments Business Operator (“FIBO”) under the registration entry Director General of the Kanto Local Finance Bureau (FIBO) No. 2414.

For Investors in Hong Kong S.A.R.: This document is being issued by MetLife Investments Asia Limited (“MIAL”), a part of MIM, and it has not been reviewed by the Securities and Futures Commission of Hong Kong (“SFC”). MIAL is licensed by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities.For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

1 MetLife Investment Management (“MIM”) is MetLife, Inc.’s institutional management business and the marketing name for subsidiaries of MetLife that provide investment management services to MetLife’s general account, separate accounts and/or unaffiliated/third party investors, including: Metropolitan Life Insurance Company, MetLife Investment Management, LLC, MetLife Investment Management Limited, MetLife Investments Limited, MetLife Investments Asia Limited, MetLife Latin America Asesorias e Inversiones Limitada, MetLife Asset Management Corp. (Japan), and MIM I LLC and MetLife Investment Management Europe Limited.