Corporate Private Credit Market1

Origination Surges on Larger Deals

- Through September 30, market origination surged to $94.7 billion in 2024 vs $62 billion in first half of 2023.

- As issuers raise larger deals, average transaction size rose to $359 million across 264 transactions YTD.

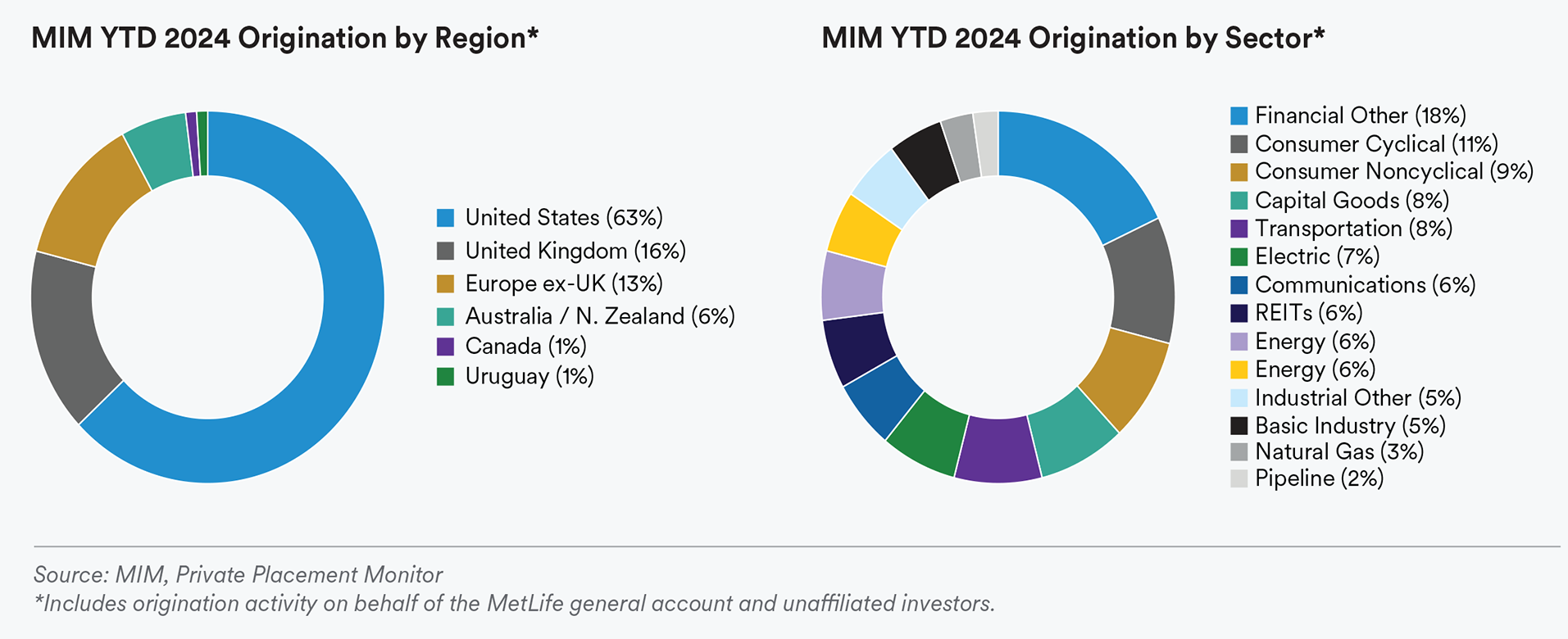

- North America led in volume with 72% of total issuance, followed by Europe at 22%, Australia at 4% and LatAm at 2%.

- Majority of issuance was in USD at 76%, followed by 10% in Euro, 7% in CAD, 5% in GBP and 2% in other currencies.

- The trend of delayed fundings was low at 6%.

- Spreads Unchanged, Treasuries Tighten

- Public spreads were relatively unchanged from Q2, tightening 5 bps with an ending OAS at +89bps.

- The 10-year UST had another active quarter, as yields tightened 70 bps to end Q3 at 3.79%.

- We expect the Federal Reserve to reduce the Fed funds rate to a 4.50-4.75% range by year-end.

MIM Corporate Private Credit Activity

- MIM’s origination through September 30, totaled $4.7 billion.

- Deal momentum tripled vs Q3 2023.

- We are seeing an uptick in market activity as interest rates has come off recent highs.

- We expect this market momentum to continue into Q4, but remain cautious about potential volatility around the U.S. election.

MIM’s Year-End Outlook

- The private market continues to post record issuance and is on pace for a solid year. We expect it to be resilient amid economic uncertainty around the U.S. election.

- Election-related volatility could offer an opportunity to take advantage of favorable pricing dynamics.

- MIM is well-positioned to leverage our underwriting experience, issuer relationships and stable private platform to capitalize on market opportunities.

Infrastructure Debt Market

Significant Global Activity, Strong Year-End Outlook

- Q3 2024 saw significant global activity in infrastructure debt, with a strong outlook for Q4.

- Megatrends such as decarbonization and digitalization continue to fuel demand for infrastructure finance.

- We expect the need for infrastructure capital to continue to grow, driven by global demand for new infrastructure and projects supporting new technologies.

- Agented deal flow continues to be complemented by strong issuance of bilateral, directly-sourced transactions.

- Expectations for the year remain positive, with a number of transactions in active dialogue and a strong pipeline of opportunities across core infrastructure sectors.

Origination Rises 83%, Well Diversified

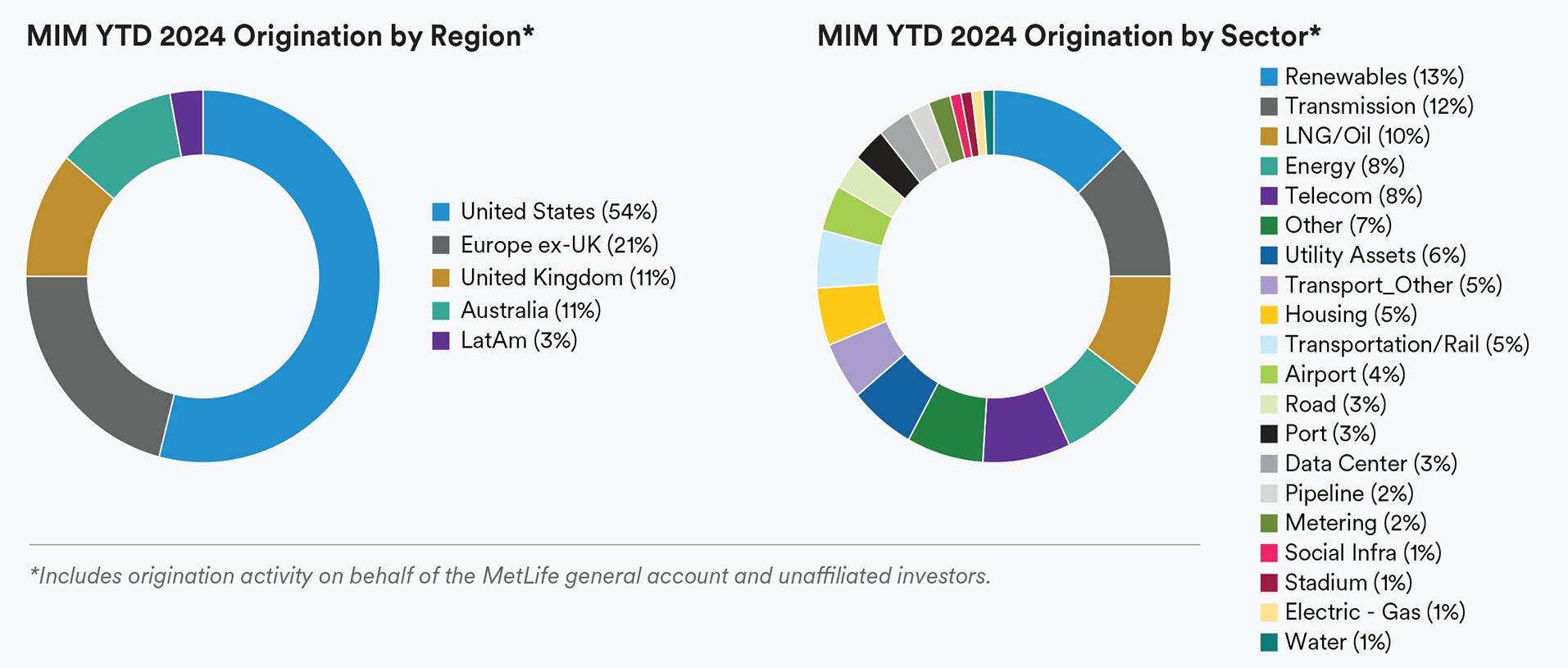

- Origination volume totaled $4.4 billion as of end of September, a steep increase over $2.4 billion in the same period last year.

- Transactions MIM originated were well diversified across all project types, led by renewables, transmission, LNG and digital.

- With strong demand from investors globally and a competitive market, MIM’s focus is on infrastructure partner relationships and targeting bilateral and direct deals.

- MIM’s global footprint and ability to source unique bilateral transactions enable us to secure attractive investment opportunities for our clients.

- Origination outside the U.S. reached 46% of infrastructure investment volume in 2024.

MIM’s Year-End Outlook

- We continue to see diversified global opportunities, from decarbonizing energy and transport to advancing communications to enhancing critical social infrastructure.

- Proprietary deal flow remains very strong, as sponsors continue to value certainty of execution and reliable partners for M&A, refinancing and Capex needs.

- As the need for infrastructure private capital continues to grow, MIM is well positioned as an experienced global lender to provide tailored solutions that support financing needs via long-term partners.

- While global competition for infrastructure assets has increased, we remain disciplined in analyzing and negotiating deal structure, focused on relative value across all investments.

- High selectivity, disciplined underwriting and solid structures are cornerstones to ensure resilience as MIM builds a client portfolio of private infrastructure debt transactions.

Private Structured Credit Market1

Sideways Movement, Robust Demand in Q3

- Esoteric ABS spreads moved within a narrow range of low-mid 200 bps in Q3.

- Investor demand was robust and should remain so into 4Q, limiting spread widening unless a market risk-off event dampens investor sentiment.

- Spreads have remained near the tight end of the 52- week range.

MIM’s Outlook

- New macro data reflects a rise in delinquencies in autos, credit cards and installment loans, particularly in lower FICO segments, while prime borrowers remain stable.

- ABS performance can diverge from broader macro data due to ABS issuers imposing tighter credit standards vs overall market.

- Consumer credit performance metrics remain rangebound; delinquencies and charge-offs are trending near long-term averages.

- Deal structural features offer significant protection against a macroeconomic downturn.

- Corporate revenue and earnings have displayed resilience into the fed rate hike cycle, supporting private equity portfolio company valuations and keeping fund finance LTVs stable.

- Anticipated fed rate cuts are likely to provide relief to both consumer and commercial ABS borrowers, which should support fundamental performance.

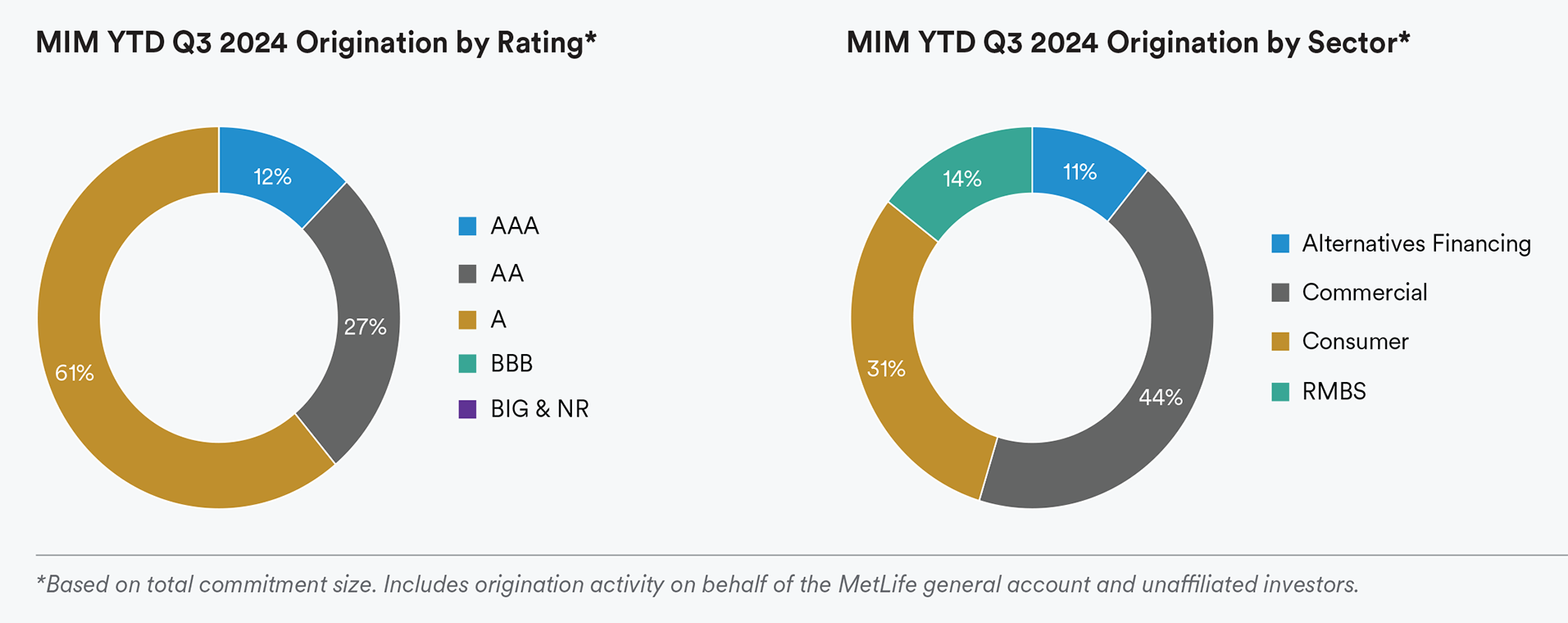

MIM Committed Transaction Activity

- MIM activity for Q3 was strong with $818 million in committed investments in the commercial, residential and alternatives financing sectors.

Endnotes

1. MetLife Investment Management, Private Placement Monitor Credit quality assessments were performed internally by MIM and have not been verified by independent sources. Any internal ratings (i.e., MetLife ratings) presented in this document were developed internally by MIM. Such ratings are not recognized ratings used by other investment managers or funds, including those investing in the sectors in which MIM invests. Other ratings, including those published by an independent credit ratings agency, may be more relevant in evaluating creditworthiness or may present the credit quality of issuers or assets in a more or less favorable manner than such internal ratings do. MIM’s internal ratings are subjective; MIM has an incentive to assign internal ratings in a manner that more closely meet investor and/or yield expectations, or otherwise provides an advantage to MIM. Accordingly, such internal ratings should be viewed as one factor among other factors for evaluating creditworthiness, and you should make your own determination as to the weight you place on such internal ratings. Please contact MIM for additional information on how such ratings are derived.

Disclosure

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors. This document has been prepared by MetLife Investment Management (“MIM”)1 solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Property is a specialist sector that may be less liquid and produce more volatile performance than an investment in other investment sectors. The value of capital and income will fluctuate as property values and rental income rise and fall. The valuation of property is generally a matter of the valuers’ opinion rather than fact. The amount raised when a property is sold may be less than the valuation. Furthermore, certain investments in mortgages, real estate or non-publicly traded securities and private debt instruments have a limited number of potential purchasers and sellers. This factor may have the effect of limiting the availability of these investments for purchase and may also limit the ability to sell such investments at their fair market value in response to changes in the economy or the financial markets.

In the U.S. this document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor.

For investors in the UK, this document is being distributed by MetLife Investment Management Limited (“MIML”), uthorized and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address One Angel Lane 8th Floor London EC4R 3AB United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as per the retained EU law version of the same in the UK.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Investment Management Japan, Ltd. (“MIM JAPAN”), a registered Financial Instruments Business Operator (“FIBO”) conducting Investment Advisory Business, Investment Management Business and Type II Financial Instruments Business under the registration entry “Director General of the Kanto Local Finance Bureau (Financial Instruments Business Operator) No. 2414” pursuant to the Financial Instruments and Exchange Act of Japan (“FIEA”), and a regular member of the Japan Investment Advisers Association and the Type II Financial Instruments Firms Association of Japan. In its capacity as a discretionary investment manager registered under the FIEA, MIM JAPAN provides investment management services and also subdelegates a part of its investment management authority to other foreign investment management entities within MIM in accordance with the FIEA. This document is only being provided to investors who are general employees’ pension fund based in Japan, business owners who implement defined benefit corporate pension, etc. and Qualified Institutional Investors domiciled in Japan. It is the responsibility of each prospective investor to satisfy themselves as to full compliance with the applicable laws and regulations of any relevant territory, including obtaining any requisite governmental or other consent and observing any other formality presented in such territory. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

For Investors in Hong Kong S.A.R.: This document is being issued by MetLife Investments Asia Limited (“MIAL”), a part of MIM, and it has not been reviewed by the Securities and Futures Commission of Hong Kong (“SFC”). MIAL is licensed by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

MIMEL: For investors in the EEA, this document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorized and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. The investment strategies described herein are directly managed by delegate investment manager affiliates of MIMEL. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are directly contracted with MIMEL or are regulated in Ireland. Unless otherwise stated, any industry awards referenced herein relate to the awards of affiliates of MIMEL and not to awards of MIMEL.

1. MetLife Investment Management (“MIM”) is MetLife, Inc.’s institutional management business and the marketing name for subsidiaries of MetLife that provide investment management services to MetLife’s general account, separate accounts and/or unaffiliated/ third party investors, including: Metropolitan Life Insurance Company, MetLife Investment Management, LLC, MetLife Investment Management Limited, MetLife Investments Limited, MetLife Investments Asia Limited, MetLife Latin America Asesorias e Inversiones Limitada, MetLife Investment Management Japan, and MIM I LLC, MetLife Investment Management Europe Limited and Affirmative Investment Management Partners Limited.