Every four years, people around the world come together to watch the beautiful game at the FIFA World Cup. For institutional investors, however, the action takes place behind the scenes, in the financing that underpins modern sports.

The real investable story in sports is not game-day performance, but the contracted, diversified cash flows that power the game. Professional sports have evolved into a capital-intensive industry supported by long-dated contracts, scarce assets, and loyal, engaged audiences. Stadiums have become multi-use infrastructure platforms engineered to generate revenue 365 days a year, while clubs, teams, and leagues increasingly resemble regulated operating businesses monetizing one of the last forms of truly live media. Broadcasting rights, sponsorships, premium seating, and experiential offerings now drive economics as much as on-field performance.

Private capital has long played a role in this ecosystem, but the opportunity has changed materially as sports organizations professionalize and revenue streams expand. Private infrastructure debt and private placements offer investors access to long-duration, diversified income streams that are structurally different from traditional corporate credit, provided that risks are carefully underwritten.

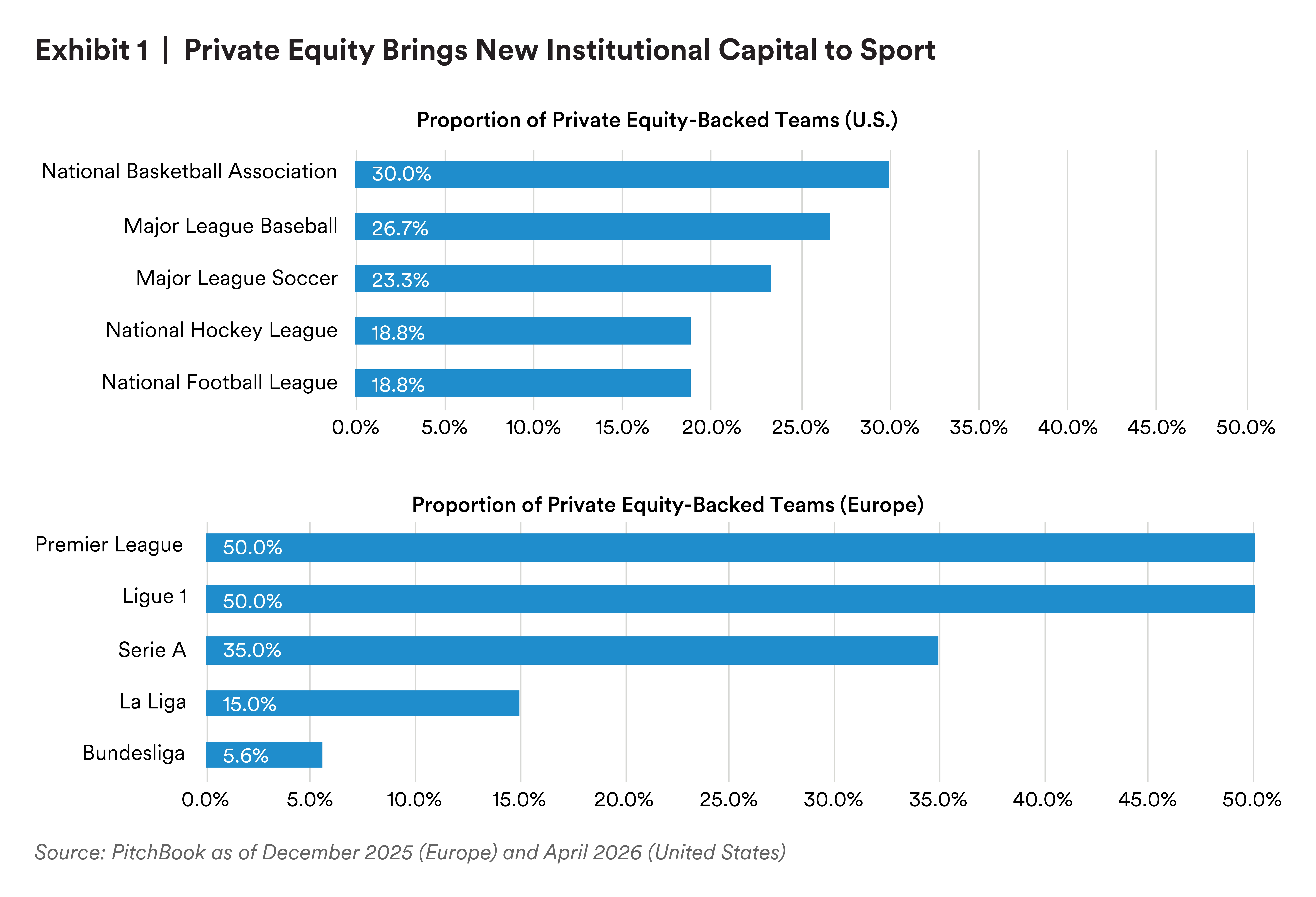

Over the last few years, institutional capital has poured into sports clubs, teams, and leagues in the United States and Europe, much of it from private equity sponsors (Exhibit 1). The door to private equity opened first in Europe in 2006, when a consortium of three investors bought the Paris St. Germain football club. The industry gained a toehold in professional sports in the U.S. in 2019, when Major League Baseball allowed teams to sell minority stakes to institutional investors. The other American leagues followed.

Over the last few years, most of the largest private equity players have announced dedicated vehicles for sports financing and made major purchases. To name a few examples, CVC Capital Partners launched a $14 billion private equity platform dedicated to sports in 2025, KKR acquired the institutional sports investment firm Arctos Partners in February 2026, and the U.S. investment bank William Blair announced an agreement to acquire Inner Circle Sports, an investment bank focused on sports, media, and entertainment, in May 2026.

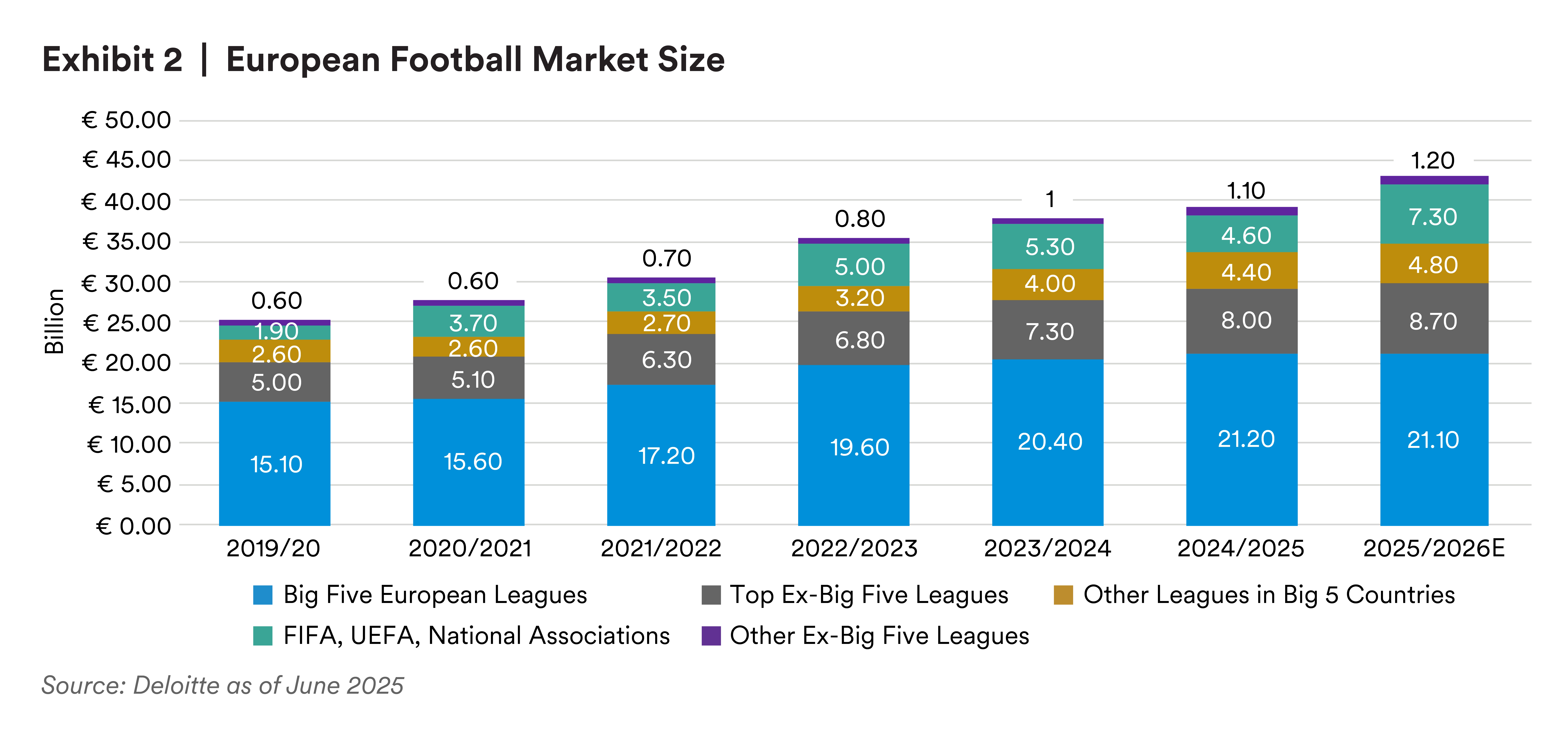

The reason for this influx is simple: Sports teams are getting more valuable, thanks to both media broadcast rights and increasingly professional operations that take every opportunity to monetize brands and slim down costs (Exhibit 2).

At a time when most people’s attention is divided across different screens and apps, television ratings are declining. In the United States, broadcast and cable viewing have declined 21% and 39%, respectively, since 2021, and streaming surpassed their combined viewership for the first time ever in 2025.1 The trends are similar in Europe, with broadcast viewership declining 4% in 2024 alone in the United Kingdom.2

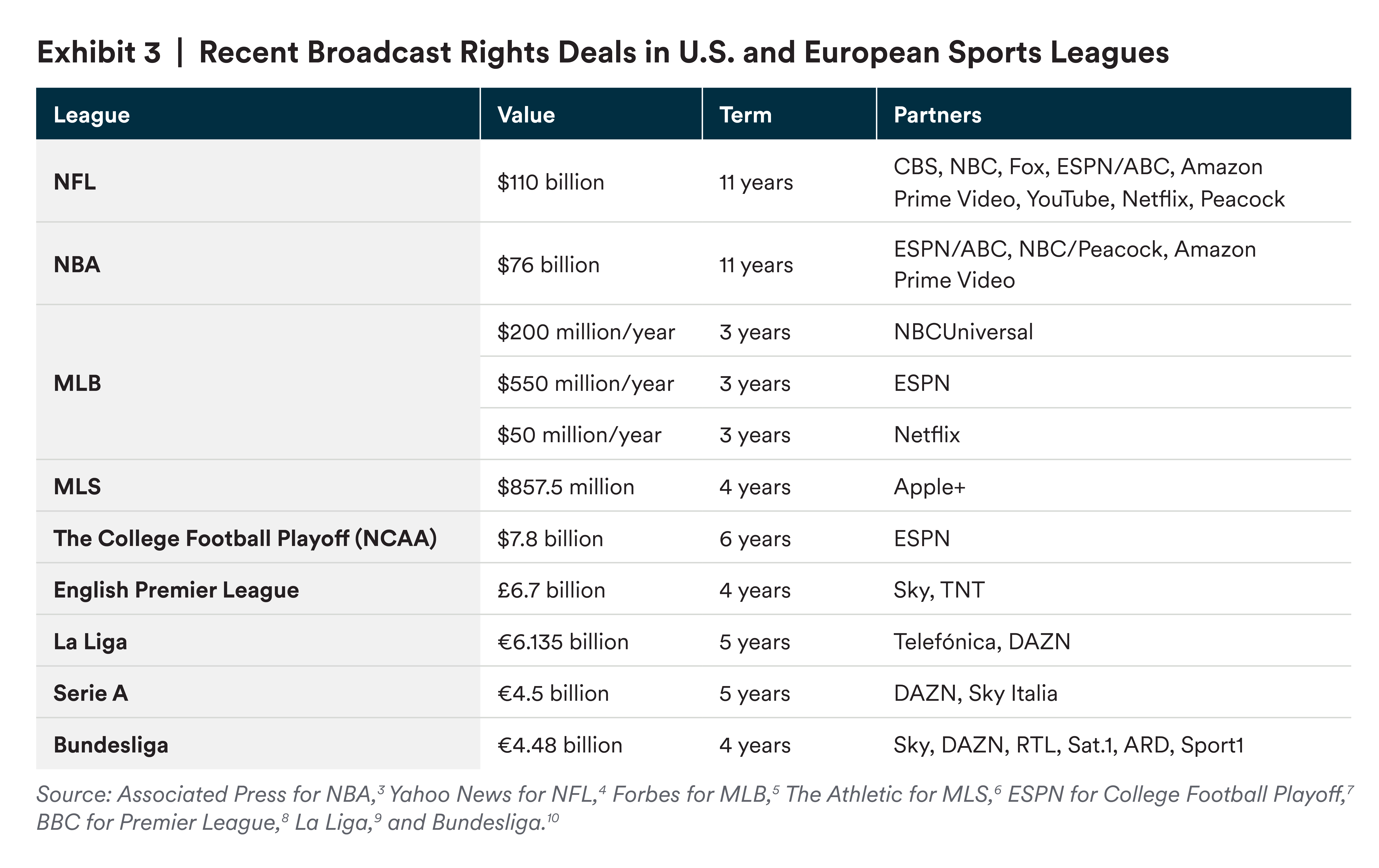

Sports events are some of the last must-see events that reliably draw a large audience. The value of broadcasting rights reflects the value that unique market position holds for advertisers (Exhibit 3).

“Sports are the last bastion of live media,” said Dillon Malandro, who covers corporate private placements for North American sports leagues on MetLife Investment Management’s Private Credit team. “The bidding wars [to air the games] have gotten so tight — not just between traditional counterparties, but also streaming services — that the intrinsic value of these contracts just soared. Everyone wants a piece of the pie.”

Private equity’s entry into sports financing is new, driven by these broadcasting streams, but private capital in sports is not. MetLife Investment Management has provided capital for teams, clubs, and leagues to refinance, expand operations, and cover expenses for at least 20 years.

For teams, clubs, and leagues, private capital may offer greater speed and certainty of execution than traditional bank lending. Private lenders may also be able to offer more bespoke terms based on the needs of the organization.

For debt investors, the potential advantages are myriad:

- Diversification: The revenue drivers of clubs, teams, and leagues are different than those of almost any other corporation, which offers investors a source of uncorrelated income in their debt allocations.

- Long-term value: The value of sports broadcasting to advertisers has proven resilient, enduring through the COVID-19 pandemic and the recovery, as well as the rise of social media and streaming media. In fact, while a proliferation in broadcasters has fragmented audiences for many traditional shows and movies, it has driven up the value of sports airtime rather than eroding it.

- Scarcity: The number of teams and clubs is strictly limited, with high barriers to forming new ones, protecting the value of existing teams.

- Senior position: The types of private placements MetLife Investment Management takes part in typically occur in the senior part of the capital structure, with cushion from both junior debt and equity.

- Contractual cash flows: In private placements, lenders tend to have first rights to revenues from multi-year media broadcasting rights contracts. The media companies in these agreements tend to be investment-grade entities. In the United States, private placements may also come with recourse to ownership stakes.

- Risk mitigation: Private placements may include debt service coverage ratio requirements, overall leverage limits, credit rating maintenance requirements, restrictions on new borrowing above a certain level, and more bespoke covenants. In one deal with a U.S. sports league, the loan stipulated that the value of the loan collateral would change if the average sales price of teams dropped below a certain threshold. In another, the contract stated that debt payments would increase if strikes or labor disputes interrupted operations for a certain period.

- Regulation: Many leagues in the United States impose strict debt limits on teams and borrow on behalf of multiple teams at once through a trust structure, reducing the risk of lending to any one team. European leagues are increasingly introducing rules intended to promote financial stability, typically achieved through limits on squad costs as a percentage of revenues, and proof-of-solvency requirements.

There are also risks and considerations. Relegation, in which the worst-performing European football clubs are demoted to lesser leagues, can materially impact the club’s broadcasting, commercial and matchday revenues, and ultimately their ability to service debt. Sporting performance is ultimately a key credit consideration both in Europe and the United States.

Assessing downside risk includes considering the long-term appeal of a team’s brand alongside performance, however. For instance, global institutions such as Real Madrid or the New York Yankees are viewed as more resilient commercial propositions, relative to lesser-known teams in smaller markets. That doesn’t mean lending to teams in newer sports or smaller markets is impossible, but a creditor would typically set stricter terms for doing so. “We are disciplined in where we put money to work,” said Alex George, a Director on the MetLife Investment Management Private Infrastructure Debt and Project Finance team in London. “While you want to get money out the door in a competitive lending environment, you also want to get it back.”

While aided by increasing professionalization across global sports, MIM’s underwriting teams pay close attention to governance risks, which remain a feature of some markets. Ensuring that a strong management team is in place, with transparency into funding and operations, is a critical consideration across all transactions.

For those who think of infrastructure in terms of the electrical grid, airports, and toll roads, stadiums might seem an odd fit at first. However, they meet our Private Infrastructure Debt team’s definition of infrastructure: discrete physical assets that generate contractual, inflation-linked cash flows, have high barriers to entry, and perform an essential service.

Those who would debate the last point better not do so in Barcelona, home of the renovated, 95,000-seat Camp Nou stadium. “There’s a saying that families go to church on Sunday morning and to watch football on Sunday evening,” said Kashif Khan, a Senior Director of Infrastructure and Project Finance at MetLife Investment Management. From Chelsea’s Stamford Bridge stadium in West London to the San Siro stadium in Milan (also due to be demolished and redeveloped this summer), European stadiums are often centrally located or easily reached by public transit—integral to cities geographically as well as emotionally.

In the United States, stadiums are often the linchpins of large, mixed-use development projects. Los Angeles Rams owner E. Stanley Kroenke is developing the area around the state-of-the-art SoFi Stadium, which will hold eight FIFA World Cup games this year, into a 289-acre sports and entertainment zone, with luxury apartments, stores, a movie theater, and a concert hall. U.S. municipalities hoping to attract jobs and visitors often contribute public funds to finance stadiums or the infrastructure around them. The City Council in Washington, D.C., invested $515 million in a public-private partnership to expand and improve the Capital One Arena and the surrounding area, for example.

Many stadiums in Europe and the United States are more than 20 years old – with some over 100 – and due for a refresh. New and renovated stadiums are designed to maximize revenues as multi-use buildings that host multiple teams and non-sports events throughout the year, with every possible square inch monetized.

Year-Round Stadiums Look Beyond Game Day

Today’s stadiums often play host to multiple teams, increasing the number of game days (Exhibit 4). In Europe, many stadiums built primarily for men’s football clubs also host women’s football matches.

Concerts and other entertainment events have become increasingly important revenue streams. “There has been huge a surge in demand for live music post-Covid,” said Kathryn Bai, a Director on MetLife Investment Management’s Infrastructure and Project Finance team. “When top artists including Beyoncé and Taylor Swift were on tour, event revenues at some stadiums even doubled.” Stadiums host family events, monster truck rallies, corporate conferences and more to maximize stadium usage and keep the concessions flowing.

Unique, on-site experiences also attract visitors. The Bernabéu Tour at Real Madrid’s new stadium will feature a bigger museum with interactive virtual reality technology and a panoramic tour. At Tottenham Hotspur Stadium in London, visitors can drive “F1-inspired karts” or strap on a safety harness for a walk out on The Dare Skywalk 46.8 meters above the pitch.

The importance of attractions and non-sports events to overall revenues varies by stadium. Its location in Las Vegas, one of the entertainment capitals of the world, affords many opportunities to host non-sports events at Allegiant Stadium, including multi-day megaevents such as WrestleMania. Credit teams at MetLife Investment Management factor all of this in when considering a stadium’s revenue streams.

Corporate Sponsorships and Naming Rights

MetLife Stadium in East Rutherford, N.J., is home of the New York Giants, New York Jets, and eight FIFA World Cup games (including the final) this year. It’s also a close-to-home example of how stadiums earn revenue from selling their names. Typically, naming rights deals last a decade or more, offering years of predictable revenue streams that can reach into the hundreds of millions of dollars. Stadium lenders often have claims on these cash flows in the event the team or club defaults.

In Europe, only one-third of the 36 clubs profiled in a recent study had sold naming rights to their stadiums, though this is changing fast, Khan says. All but four Bundesliga stadiums in Germany have corporate sponsors, for example, including the Allianz Arena where Bayern Munich plays and Deutsche Bank Park in Frankfurt.

Companies also pay to name pavilions, hospitality suites, and premium seating areas. Exhibit 5 shows how this breaks down at the Climate Pledge Arena in Seattle, Washington.

Exhibit 5: Named Hospitality Sponsorships at Climate Pledge Arena

Priority Seating, Hospitality Lounges, and Personal Seat Licenses

New and renovated stadiums usually seek to add more VIP lounges, luxury boxes, corporate suites, and club seats. These premium seats, which are often locked in by multi-year contracts, can generate millions of dollars in sales. They’re also important to creditors, who often have recourse to these cash flows.

Barcelona’s new stadium will hold 9,400 VIP locations when fully completed, more than tripling hospitality capacity from the previous stadium. VIP seat licenses sell for €20,000-€80,000 each, plus annual fees, for a period of 15-30 years.12 In May 2026, the club’s website said suites, boxes, and the VIP ring of seats had already sold out, months before the stadium is fully opened.

Structuring Stadium Debt to Account for Project Finance Risk

Financing a stadium has different risks than lending money to a more traditional corporation. Stadiums are infrastructure investments, and like most infrastructure investments, debt is secured by specific contractual cash flows. These might include naming rights, sponsorships, luxury suite premiums, club seat premiums, concessions, merchandise, event rent, ticket fees, parking charges, attraction revenues, and so on.

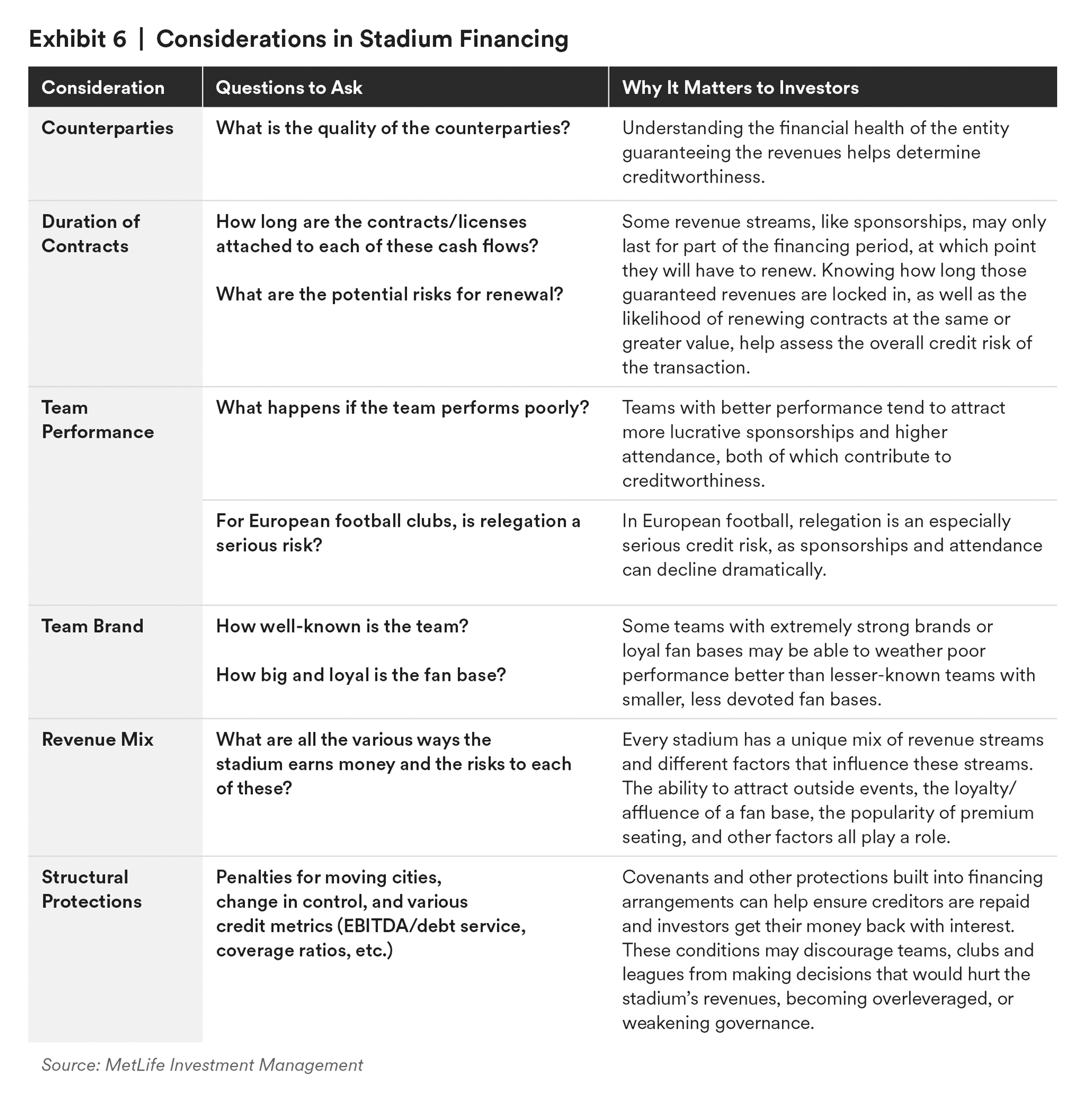

In assessing the risks and potential benefits of an investment, our team looks closely at the durability of these contractual cash flows in many different ways. (Exhibit 6).

Exhibit 6: Considerations in Stadium Financing

As the business of sports expands around the globe and into newer sports and leagues, our Private Infrastructure Debt team expects financing to follow. MetLife Investment Management recently completed a $40 million loan backed by a sponsorship agreement to support the construction of a new stadium for Denver Summit FC, a U.S. National Women’s Soccer League team.

The business of sports has outgrown the traditional narratives that once defined it. What appears from the outside to be driven by passion, performance, and fandom is increasingly sustained by long-dated contracts, diversified revenue streams, and institutional-grade governance. Stadiums now function as year-round infrastructure assets, while clubs, teams, and leagues operate as scarce, regulated platforms monetizing one of the last forms of truly live media.

For institutional investors, stadium financing and corporate private placements potentially provide access to predictable cash flows, structural protections, and senior positioning in capital structures that have in some cases demonstrated a degree of resilience as capital has flowed in. For lenders with the specialized expertise and discipline to underwrite the economics beneath them, sports potentially represent a durable and evolving source of long-term value.

MetLife: A Long-Term Partner to Sports Organizations

With more than $2 billion in stadium loans and over $3 billion in corporate private placements outstanding, MetLife Investment Management is one of the largest private debt providers in professional sports.

Our parent company, MetLife, sponsors the Japan Futsal National Team and the Men’s, Women’s and Youth National Football Teams in Mexico.

Endnotes

1 Nielsen. “Streaming Reaches Historic TV Milestone, Eclipses Combined Broadcast and Cable Viewing for First Time.” June 2025. https://www.nielsen.com/news-center/2025/streaming-reaches-historic-tv-milestone-eclipses-combined-broadcast-and-cable-viewing-for-first-time/

2 Ofcom. “Media Nations: UK 2025.” https://www.ofcom.org.uk/siteassets/resources/documents/research-and-data/multi-sector/media-nations/2025/media-nations-2025-uk-report.pdf?v=401287

3 Tim Reynolds and Joe Reedy. “NBA agrees to terms on a record 11-year, $76 billion media rights deal, AP source says.” Associated Press, July 10, 2024. https://apnews.com/article/nba-media-deal-tv-07d021c1248bedfe547885a54f0b3f32?utm_source=copy&utm_medium=share

4 Kayla Cobb. “The $110 Billion Squeeze: How NFL’s Seismic Cash Grab Could Reshape TV.” Yahoo News, May 6, 2026. https://sports.yahoo.com/articles/110-billion-squeeze-nfl-seismic-130000660.html

5 Maury Brown. “MLB Agrees To 3-Year Media Rights Deals With ESPN, NBCUniversal And Netflix.” Forbes, November 19, 2025. https://www.forbes.com/sites/maurybrown/2025/11/19/mlb-announces-3-year-media-rights-deals-with-espn-nbcuniversal-and-netflix/

6 Paul Tenorio. “MLS, Apple rework terms of media rights deal for earlier ending, in 2029.” The Athletic, November 14, 2025. https://www.nytimes.com/athletic/6808440/2025/11/14/mls-apple-tv-broadcast-rights-deal-2029/

7 Heather Dinich. “College Football Playoff, ESPN agree to deal through 2031-32.” ESPN, March 19, 2024. https://www.espn.com/college-football/story/_/id/39766079/college-football-playoff-espn-agree-deal-2031-32

8 BBC. “Premier League Agrees Record £6.7bn Domestic TV Rights Deal.” December 4, 2023. https://www.bbc.com/sport/football/67619756

9 La Liga. “LALIGA Secures over €6.135 Billion in Domestic Audiovisual Revenue for 2027/28–2031/32, up 9% over Previous Cycle.” November 28, 2025. https://www.laliga.com/en-GB/news/laliga-secures-over-euro6135-billion-in-domestic-audiovisual-revenue-for-2027-28-2031-32-up-9percent-over-previous-cycle

10 Sebastian Stafford-Bloor. “The Bundesliga’s New €4.48bn TV Deal: The Details, the View in Germany and how it Compares.” The Athletic, December 6, 2024. https://www.nytimes.com/athletic/5972169/2024/12/05/bundesliga-tv-contract-analysis/

11 Kroll. “Why European Football Clubs Should Look to Stadium Naming Rights to Diversify Income.” July 23, 2024. https://www.kroll.com/en/reports/valuation/european-stadium-naming-rights-report-2024

12 FC Barcelona. “FC Barcelona Drive Forward a New Model of VIP Seats at Spotify Camp Nou and Increase Stadium Revenue Predictions.” February 24, 2026. https://www.fcbarcelona.com/en/club/news/4456324/fc-barcelona-drive-forward-a-new-model-of-vip-seats-at-spotify-camp-nou-and-increase-stadium-revenue-predictions

Disclaimer

Credit quality assessments were performed internally by MIM and have not been verified by independent sources. Any internal ratings (i.e., MetLife ratings) presented in this document were developed internally by MIM. Such ratings are not recognized ratings used by other investment managers or funds, including those investing in the sectors in which MIM invests. Other ratings, including those published by an independent credit ratings agency, may be more relevant in evaluating creditworthiness or may present the credit quality of issuers or assets in a more or less favorable manner than such internal ratings do. MIM’s internal ratings are subjective; MIM has an incentive to assign internal ratings in a manner that more closely meet investor and/or yield expectations, or otherwise provides an advantage to MIM. Accordingly, such internal ratings should be viewed as one factor among other factors for evaluating creditworthiness, and you should make your own determination as to the weight you place on such internal ratings. Please contact MIM for additional information on how such ratings are derived.

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors.

MetLife Investment Management (MIM), which includes PineBridge Investments, is MetLife Inc.’s institutional investment management business. MIM is a group of international companies that provides investment advice and markets asset management products and services to clients around the world.

This document is solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein.

This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

The various global teams referenced in this document, including portfolio managers, research analysts and traders are employed by the various legal entities that comprise MIM.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results.

For investors In the U.S: This document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities and Exchange Commission (SEC) registered investment adviser. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment adviser.

For investors in the UK: This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address One Angel Lane 8th Floor London EC4R 3AB United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK who qualify as a "professional client" as defined under the Markets in Financial Instruments Directive (2014/65/EU), as per the retained EU law version of the same in the UK.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Investment Management Japan, Ltd. (“MIM JAPAN”), a registered Financial Instruments Business Operator (“FIBO”) conducting Investment Advisory Business, Investment Management Business and Type II Financial Instruments Business under the registration entry “Director General of the Kanto Local Finance Bureau (Financial Instruments Business Operator) No. 2414” pursuant to the Financial Instruments and Exchange Act of Japan (“FIEA”), and a regular member of the Investment Management Association of Japan and the Type II Financial Instruments Firms Association of Japan. In its capacity as a discretionary investment manager registered under the FIEA, MIM JAPAN provides investment management services and also sub-delegates a part of its investment management authority to other foreign investment management entities within MIM in accordance with the FIEA. This document is only being provided to investors who are general employees' pension fund based in Japan, business owners who implement defined benefit corporate pension, etc. and Qualified Institutional Investors domiciled in Japan. It is the responsibility of each prospective investor to satisfy themselves as to full compliance with the applicable laws and regulations of any relevant territory, including obtaining any requisite governmental or other consent and observing any other formality presented in such territory. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

For Investors in Hong Kong S.A.R.: MetLife Investment Management and PineBridge Investments operate through the following entities: MetLife Investments Asia Limited (“MIAL”), licensed by the Securities and Futures Commission (“SFC”) for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities, PineBridge Investments Asia Limited licensed by the SFC for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities, and PineBridge Investments Hong Kong Limited licensed by the SFC for Type 1 (dealing in securities) and Type 9 (asset management) regulated activities. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are licensed by the SFC to carry on regulated activities in Hong Kong S.A.R. The information contained in this document is for information purposes only and it has not been reviewed by the Securities and Futures Commission. This document may also be distributed by certain PineBridge Investments affiliates acquired by MetLife Investment Management on December 30, 2025. For additional legal and regulatory disclosures including other cross border information, please refer to https://www.pinebridge.com/en/regulatory-disclosure.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

For investors in the EEA: This document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. The investment strategies described herein are directly managed by delegate investment manager affiliates of MIMEL. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are directly contracted with MIMEL or are regulated in Ireland. Unless otherwise stated, any industry awards referenced herein relate to the awards of affiliates of MIMEL and not to awards of MIMEL.