- MetLife Investment Management’s Secular and Economic Trends Conference (MIMSET) is a biennial conference that tracks the long-term fundamental trends shaping capital markets. The conference’s goals are to help business leaders and asset owners rethink risk, diversify portfolios, and navigate secular and economic trends during a period of rapid, often unpredictable change.

- Earlier this year, we welcomed clients to the MetLife Building in New York for a day of thought-provoking commentary on the forces that will shape the world over the next 10 years. Our guest speakers were Sir Niall Ferguson, Senior Fellow at the Hoover Institution; retired U.S. Army Maj. Gen. James Marks, Head of Geopolitical Strategy at Academy Securities; Harvard University Professor Kenneth Rogoff; and former Federal Reserve Board of Governors Vice Chair Roger Ferguson.

- Our Global Economics and Market Strategy team has processed and synthesized the discussions and incorporated them into our own forward-looking views on markets and the global economy. The views presented here are our own, but they weave in lessons, surprises, and insights from MIMSET.

Around the world, we see countries turning away from the international rules-based order that has been in place since World War II. Precisely what sort of geopolitical balance and economic system will emerge in its place remains unclear. What is clear is that investors today must examine their core assumptions, some of which haven’t been deeply challenged in decades. MIM’s Secular and Economic Trends Conference 2026 highlighted three assumptions that are particularly vulnerable in the coming decade.

Old Assumption: Economic policy trumps geopolitical considerations.

New Assumption: Geopolitics trumps economics.

National security has played second fiddle to economic policy for the last few decades, with global economic policy oriented toward globalization and reducing trade barriers. Going forward, we expect national security to increasingly shape economic policy in individual countries, thereby making the global economy more brittle and vulnerable to supply shocks. A geopolitical lens is becoming mandatory when evaluating investments.

Old Assumption: The dollar is the world’s unquestioned reserve currency.

New Assumption: The world is transitioning to a multipolar currency regime.

During times of stress in the post-war period, the dollar could be counted on to rise and U.S. Treasury yields to fall as investors sought the safety of the greenback. Now, the playbook has become more complex. Markets are increasingly reacting to shocks in idiosyncratic ways, depending on the precise nature of the event. Investors must be prepared for a variety of responses.

Old Assumption: Fiscal strength is a hallmark of developed countries.

New Assumption: Developed countries exist along a fiscal continuum.

Relatively robust balance sheets and low financing costs were once key factors separating developed markets from emerging markets. Looking ahead, developed-market finances are looking shakier. Critically, this includes the capacity to fund militaries appropriately, which has historically been associated with the erosion of power.

Replacing the old rules with these new assumptions yields a more complicated, more volatile investing environment that centers less around the United States. We’ll take a deeper dive into how these three new paradigms could affect global priorities, the dollar and the fiscal strength of the U.S. and its allies.

In our view, the post-WWII rules-based international order — particularly the efforts made to prioritize economic cooperation over military conflict — is over. Going forward, we expect geopolitics will play a greater role in shaping the global economy, as national security concerns weigh more heavily in economic and political decisions. Supply shocks are likely to feature prominently as the dependable rules of globalization give way to a more unruly and fragmented global economy.

Investors can no longer rely on economic policy to favor globalization or even domestic business interests. Conventional economic policy would not have contemplated imposing the level of tariffs the Trump administration announced on April 2, 2025, for example. The Iran conflict, too, was antithetical to near-term economic growth. While both events happened during President Trump’s second term, the shift to favoring national security over the best interests of domestic businesses started before his re-election. President Biden retained tariffs on China from the first Trump presidency and signed the 2022 CHIPS and Science Act, a national security initiative, which funded incentives for expanding domestic manufacturing of critical technology and advanced semiconductor research. Regardless of who the next president is or the composition of the next Congress, we expect national security to feature more prominently in U.S. policy going forward.

As the CHIPS Act demonstrates, industrial policy has re-emerged as an outgrowth of national security concerns. As the U.S. military’s attention and resources appear increasingly stretched among competing geopolitical priorities, the pressure to shore up domestic production capabilities intensifies. Sir Niall Ferguson, Senior Fellow at the Hoover Institution, describes the U.S. military’s juggling act as a “three-bodies-of-water problem.” The U.S. had, in prior eras, been able to assert its military authority in two of three critical regions simultaneously: the Persian Gulf; the North Atlantic, including Europe, Russia and part of Africa; and Asia Pacific. Both Ferguson and retired U.S. Army Maj. Gen. James Marks, Head of Geopolitical Strategy at Academy Securities, believe budget constraints leave the U.S. able to assert its military authority in only one region at a time.

In this new reality, international institutions and a flexible global marketplace are likely to be a less effective buffer against supply shocks. When supply shocks happen inside a more rigid and brittle system, they are likely to create inflation and rate pressures that are harder to manage than those of classic demand shocks. The typical responses of fiscal stimulus and rate cuts may not be sufficient, and countries working in their own self-interest may leverage geographic, economic, and technological advantages in ways that previously would have been unthinkable. The unilateral way in which the U.S. imposed tariffs (plus China’s retaliation, Exhibit 1) and Iran’s move to close the Strait of Hormuz are prime examples. This, combined with less international policy coordination, has the potential to increase the frequency of supply shocks.

All else being equal, countries intervening in markets to gain a perceived national security advantage would tend to reduce global productivity. Tariffs and industrial policy can impede the efficient allocation of capital — and while productivity-boosting trends such as the implementation of AI may counter productivity losses, these types of policy interventions remain an economic headwind.

If geopolitics trumps economics, a geopolitical lens on investment decisions becomes mandatory. Understanding and integrating national security concerns of key global powers into investment decisions is increasingly becoming table stakes for institutional investors. Regional and bloc-based diversification may become increasingly important and could supplant traditional global diversification strategies.

We also think investors will have to grapple with major structural changes to the rhythms of the global economy. The business cycle may no longer be the primary organizing principle of investment decisions. Supply shocks are likely to become a key organizing principle, as they are likely to increase as nations pursuing their individual national interests come into conflict with the reality of global supply chains. Inflation may increasingly fluctuate outside the traditional business cycle. Real assets with inherent value, such as commodities, land, and infrastructure, become increasingly important in this kind of environment.

More concretely, national priority sectors—defense, semiconductors, energy infrastructure, logistics and cybersecurity—may hold greater value, all else being equal. Company-specific exposure to supply chain risks and regional risks is likely to remain at least as important as they were during the COVID pandemic.

There has been increasing disquiet among countries in recent years about their reliance on the U.S. dollar. Sovereign ratings downgrades, struggles to pass budgets, rising fiscal burdens and sanctions on Russia that leveraged the U.S.’s position at the center of global financial markets have all contributed to the unease. Indeed, the greenback’s dominance over the global financial system appears to have peaked in 2015, according to Harvard University Professor Kenneth Rogoff’s taxonomy of dollar bloc countries. Going forward, we expect the global economy to continue its efforts to reduce reliance on the U.S. dollar.

Market observers often discount this trend because they get stuck on the succession plan: The dollar must be secure in its leadership position because no other currency is currently capable of supplanting it. Professor Rogoff’s rejoinder is that there need not be a single currency that supplants a global reserve currency. Historically, there have been decades-long transition periods during which multiple important currencies co-exist. We are likely entering such a period.

The Chinese government is a prime example of how nations have been trying to reduce their exposure to aspects of the U.S. dollar regime. For the past decade, China has been working hard to reduce its U.S. Treasury holdings, support its own digital currency, extend swap lines and encourage trade invoicing in renminbi. The Chinese government has upgraded its payment rails to smooth the way for renminbi transactions. Approximately 30% of Chinese exports are invoiced in local currency, up from very low levels a decade ago.

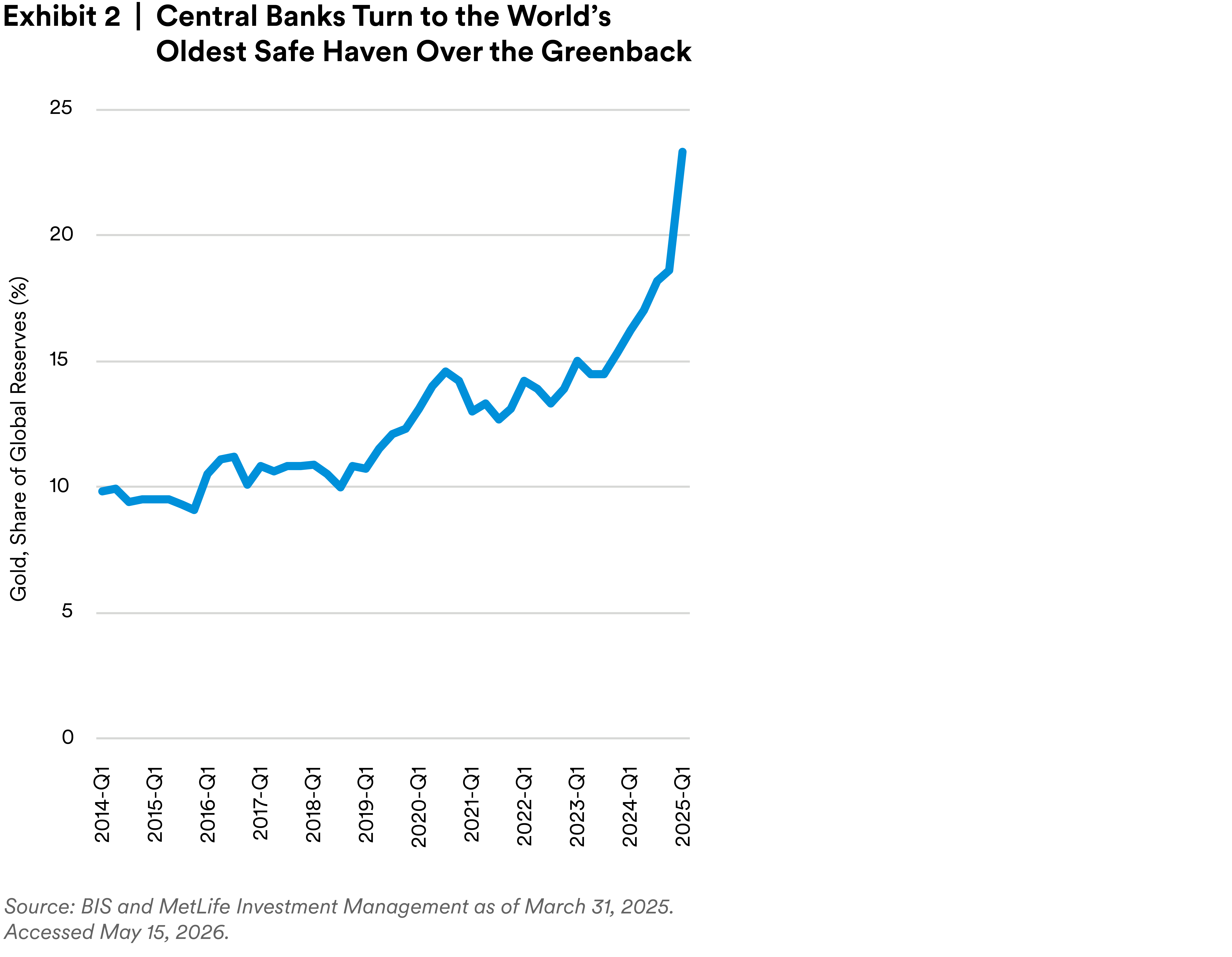

To our earlier point, geopolitical considerations are often at the heart of de-dollarization. The stringent U.S. sanctions against Russia after the 2022 invasion of Ukraine caused a number of countries to diversify their foreign holdings. President Trump’s comments about annexing Greenland appear to have lit a fire in Europe to safeguard the region’s interest, including improving euro payment rails to support greater cross-border euro usage. Finally, global central banks have been adding to their gold reserve positions over the past few years, seeking out an alternate safe haven (Exhibit 2). Cryptocurrencies appear to have found a niche in conducting cross-border transactions that require discretion and had previously been done in U.S. banknotes.

We are not yet at a critical point: The dollar is still the dominant currency and is likely to remain so for a long time. But reserve dominance can persist even as safe-haven behavior becomes less reliable. Hints of trouble are already appearing in the U.S. Treasuries. Treasuries, particularly since the April 2025 “Liberation Day” tariff announcement, have started to behave less like safe-haven assets during times of stress. That means the financing discount that Treasuries have enjoyed as the predominant safe-haven asset is under threat. Demand for U.S. Treasury debt could fall as foreign entities reduce their exposure to U.S. government debt.

Markets appear to increasingly differentiate between U.S. Treasuries and U.S. risk assets, or the equity and debt of U.S. firms, which remain very much in favor (Exhibit 3). Former Federal Reserve Board of Governors Vice Chair Roger Ferguson noted that the U.S. financial sector remains extraordinarily diversified and deep. The U.S. economy remains far more dynamic relative to other developed markets—captured by the relentless strength of U.S. private sector innovations (Exhibit 4).

The rise of a multipolar currency regime will likely drive changes in existing correlations among global assets. As investors question the U.S. as a safe haven, the behavior of U.S. Treasuries and the dollar during risk events is becoming less predictable. Risk-off trades may look less like a rush to U.S. Treasuries and more like a diffuse flow into a broader basket of assets—including U.S. investment-grade assets, real assets and sovereign debt—whose precise composition depends on the specific risk-off situation.

Furthermore, investors need to distinguish more clearly between various types of dollar exposure. U.S. Treasuries, currency risk and U.S. corporates each represent a different set of risks, with different levels of exposure to a shift toward multipolarity.

We are growing increasingly concerned about the fiscal condition of some developed economies, where the capacity to reliably repay debt while maintaining an adequate level of spending is coming into question.

Such questions have come up before. Japan spent decades struggling with its debt overhang, and the U.S. has struggled to keep its government funded and out of technical default during shutdowns and debt ceiling negotiations. The eurozone debt crisis followed the Global Financial Crisis, and the U.K. had a meltdown in 2022 after the government announced large, unfunded tax cuts. Still, we find the current fiscal situation particularly worrying for a few reasons.

First, the debt burden is much higher now than it was in past crises. The stressors of the 2008 financial crisis and the 2020 pandemic led to a large debt increase in the U.S., Japan, Germany, France and U.K. Of these, only Germany has a debt-to-GDP ratio close to that which it had in 2007. Most other large nations have struggled to reduce their debts. Rising global interest rates have also increased interest payments in most countries.

Second, in the current geopolitical environment, today’s debt troubles are likely to collide head-on with increasing militarization. The “peace dividend” following the Cold War appears to have run its course. Russia’s aggression in Ukraine, Europe’s lack of preparedness for such a conflict, U.S. insistence that allies such as NATO member states build greater military capacity, and the rapid drawdown of ammunition stockpiles during both the Ukraine and the Iran conflict all point to the need for individual countries to spend more on their militaries.

Some are already doing so. Military spending as a share of GDP has grown in Japan, Russia and some European countries in recent years. The Trump administration is looking to boost military spending, which would begin to raise military spending as a share of GDP from its current historic lows.

Sir Niall Ferguson has proposed “Ferguson’s Law,” which compares military expenses and interest expenses. According to his research, a country historically struggles to project power when it faces a high debt burden. Put another way, historically, an extended period in which interest payments are higher than military expenditures threatens a country’s ability to remain a great power. Based on this law, few countries are in a sufficiently robust economic position to project military power, including the U.S. (Exhibit 5). The apparent exceptions are Germany and South Korea. Russia’s data are somewhat spotty, but its aggregate debt burden does appear to be relatively low (Exhibit 6).

Greater fiscal pressure among developed countries creates heightened uncertainties around sovereign yields, the fiscal consequences of military spending, and possibly even the commitment to 2% inflation. Developed market countries may be pushed to finance increases in defense spending with fiscal space they do not really have, creating new and potentially destabilizing strains in sovereign debt markets that investors will need to watch closely. Developed market sovereign analysis may increasingly require an emerging-markets framework focused on debt dynamics and policy credibility, and long-duration sovereign bonds may face a more persistent fiscal risk premium.

By contrast, the opportunities in emerging markets have broadened in recent years, according to Tom Smith, MetLife Investment Management Managing Director in Public Fixed Income. The overall size of these markets has grown, as has the selection of offerings—from very risky to near-investment grade. Well-organized economies with modest military requirements may prove to be an interesting source of stability.

Over the last 70 years, patterns in financial markets and economics became so reliable they felt like natural laws. But the next decade will put old investment assumptions through their paces, and we think it pays for investors to start thinking now about what happens if familiar patterns no longer hold.

As countries shift from pulling together toward globalization to prioritizing national security, investors will need to look at investments through a geopolitical lens in the same way they look at other fundamental characteristics. In a more fractious, less globalized world, supply shocks and the attendant inflation problems they cause could replace or at least contend with the business cycle and recessions as the key drivers of economic growth.

Going forward, investors also must rethink what markets will do in risk-off investment environments, as U.S. Treasuries and the dollar will no longer automatically benefit. As countries around the world reduce their dependence on the greenback, risk-off trades are becoming more complex and will need to be tailored to the specific nature of the shock. Finally, rising fiscal concerns across most developed markets mean greater caution around sovereign debt investment, military capacity and possibly even concerns about inflation reversion toward 2% by central banks.

We don’t know yet what the patterns of a more multipolar world where developed markets sit under heavier debt burdens will look like. The shape of the post-post-World War II order is still a mystery. But by questioning the old assumptions early, investors can prepare for what lies ahead and the investment opportunities that will remain even as the world changes.

Disclosure

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors.

MetLife Investment Management (“MIM”) is MetLife, Inc.’s institutional investment management business. MIM is a group of international companies that provides investment advice and markets asset management products and services to clients around the world. The various global teams referenced in this document, including portfolio managers, research analysts and traders are employed by the various legal entities that comprise MIM.

All investments involve risk, including possible loss of principal; no guarantee is made that investments will be profitable. This document is solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. Views may be based on third-party data that has not been independently verified. MIM does not approve of or endorse any republication of this material. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

In the U.S: This document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor.

For investors in the UK: This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address One Angel Lane 8th Floor London EC4R 3AB United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as per the retained EU law version of the same in the UK. © 2025 MetLife Services and Solutions, LLC.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Investment Management Japan, Ltd. (“MIM JAPAN”), a registered Financial Instruments Business Operator (“FIBO”) conducting Investment Advisory Business, Investment Management Business and Type II Financial Instruments Business under the registration entry “Director General of the Kanto Local Finance Bureau (Financial Instruments Business Operator) No. 2414” pursuant to the Financial Instruments and Exchange Act of Japan (“FIEA”), and a regular member of the Japan Investment Advisers Association and the Type II Financial Instruments Firms Association of Japan. In its capacity as a discretionary investment manager registered under the FIEA, MIM JAPAN provides investment management services and also subdelegates a part of its investment management authority to other foreign investment management entities within MIM in accordance with the FIEA. This document is only being provided to investors who are general employees’ pension fund based in Japan, business owners who implement defined benefit corporate pension, etc. and Qualified Institutional Investors domiciled in Japan. It is the responsibility of each prospective investor to satisfy themselves as to full compliance with the applicable laws and regulations of any relevant territory, including obtaining any requisite governmental or other consent and observing any other formality presented in such territory. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

For Investors in Hong Kong S.A.R.: This document is being issued by MetLife Investments Asia Limited (“MIAL”), a part of MIM, and it has not been reviewed by the Securities and Futures Commission of Hong Kong (“SFC”). MIAL is licensed by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

For investors in the EEA: This document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. The investment strategies described herein are directly managed by delegate investment manager affiliates of MIMEL. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are directly contracted with MIMEL or are regulated in Ireland. Unless otherwise stated, any industry awards referenced herein relate to the awards of affiliates of MIMEL and not to awards of MIMEL.