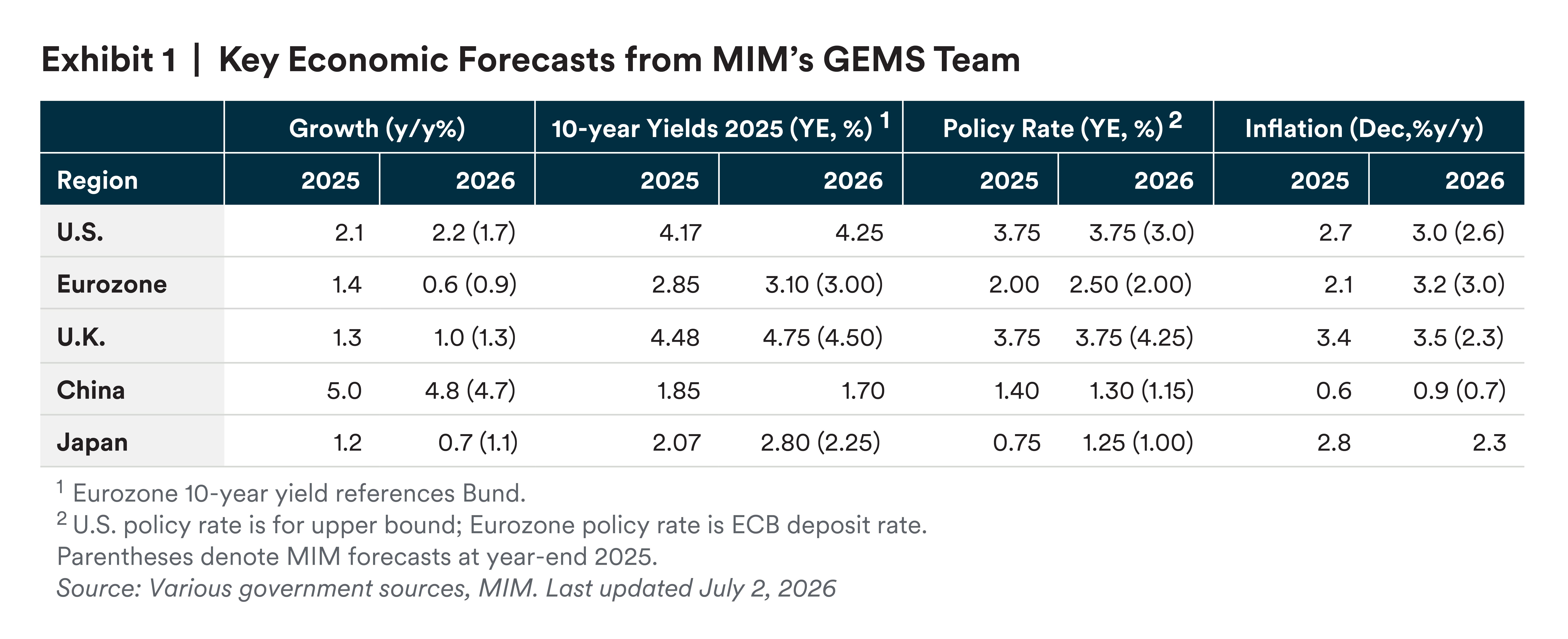

Globally, the key change in our forecasts was the unexpected conflict between the U.S./Israel and Iran , as well as its unexpected duration. As a result, we have raised our inflation forecast and our policy rate expectations, despite a decline in growth for developed markets aside from the U.S.

Our baseline expectation is that the U.S. remains the exception, handling the oil shock well and displaying above-average growth largely tied to frenetic AI-related activity. We differ from market and consensus expectations for the Fed, as we do not expect a hike in 2026.

We see three key sets of risks to these forecasts: inflation risks to the upside, a demand bust in the U.S. to the downside, and several key geopolitical risks injecting volatility.

A key set of risks to our outlook is rising inflation drivers. AI-related price increases, a longer-than-expected normalization timeline for Strait of Hormuz shipping, and more tariff policy uncertainty all have a potential inflationary effect in the next three-to-six months. If any or all of these materialize, we could see the 10-year yield drift higher, and more Fed hikes than even what the market is currently pricing in.

A second set of risks to our outlook is a large-scale pullback in demand either by consumers or by investors, particularly those in the AI space. This could either lead to recessions or a deceleration in growth that falls short of a formal recession.

Finally, we highlight a few important geopolitical tensions, including rising political tensions between the euro area and China and the possible economic risks they present.

We see the possibility of a longer-than-expected economic recovery from the U.S. conflict with Iran.

The conflict itself appears to be ebbing. Financial market concerns around inflation and supply chains appear to have disappeared upon the signing of the June 17 Memorandum of Understanding (MoU), despite its stopgap nature.

But there are numerous hurdles to overcome. Negotiations and tensions continue, and the memorandum is some distance from a finalized treaty. It is not yet clear whether negotiations will be successful, and there is a risk of the Strait of Hormuz closing again after the 60-day negotiation period.

Even if the current situation is converted into a more durable peace, the recovery process is likely to be drawn out. In no particular order:

- There are mines and a backlog of ships in the Strait that must be cleared.

- Cargo ships are out of position, and industrial equipment needs to be restarted.

- Insurance costs are likely to remain substantial.

- Infrastructure needs to be repaired.

- Prices may remain elevated while firms and governments replenish oil, gas, and other inventories.

- Authorities could implement tolls in violation of the UN Convention on the Law of the Sea – potentially opening the door to other tolls globally.

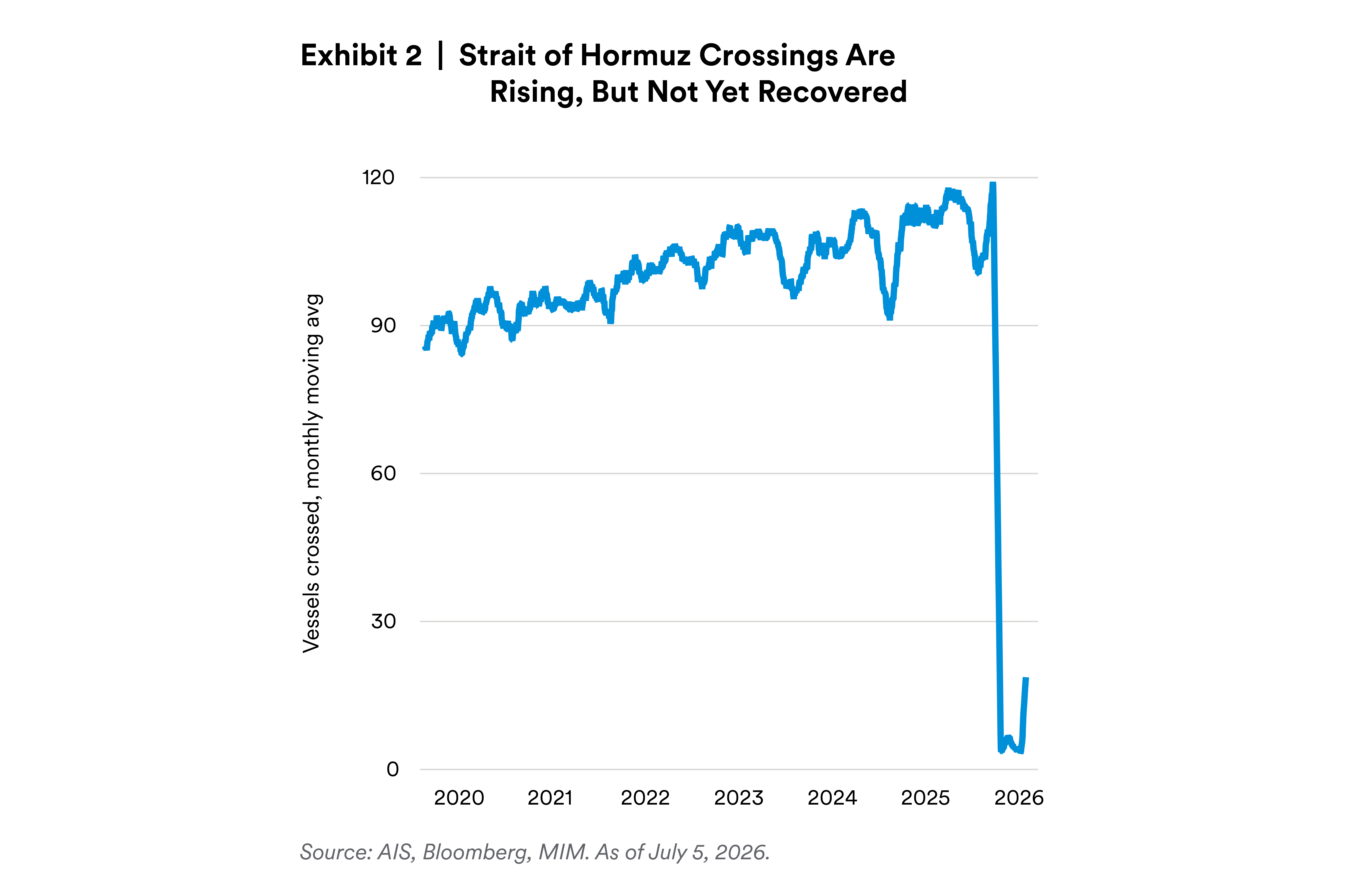

Many recovery activities are likely to keep prices elevated by supporting oil prices and higher related costs. Normalization could conceivably take many more months even assuming the MoU holds, meaning oil supplies and Strait traffic could be under pressure into 2027 (Exhibit 2).

Key implications: Under this scenario, there would be a greater likelihood for the U.S. Federal Open Markets Committee (FOMC) to hike rates by more than markets are currently pricing in. The timing may stretch out as the long tail of recovery becomes clear. The eurozone’s fragile, contingent stability rests almost entirely on the pace and permanence of the Strait of Hormuz reopening. This scenario would likely be a substantial blow to eurozone growth, with recession risks rising sharply as the scenario becomes more negative. The European Central Bank (ECB) would face a difficult path forward, partly priced into the unusually wide distribution of possible outcomes from a full pause at 2.25% to a forced tightening cycle to 3.50%. Finally, the debasement trade may be revived. Global markets moved away from the debasement trade as inflation worries dissipated. This shift away would likely prove to be premature under this longer-tail-to-recovery scenario.

AI-related firms have raised investment commitments for the year from $539 billion to $820 billion since the start of the year.1,2 IPOs and bond issuance in the sector have only raised AI firms’ capacity to spend money.

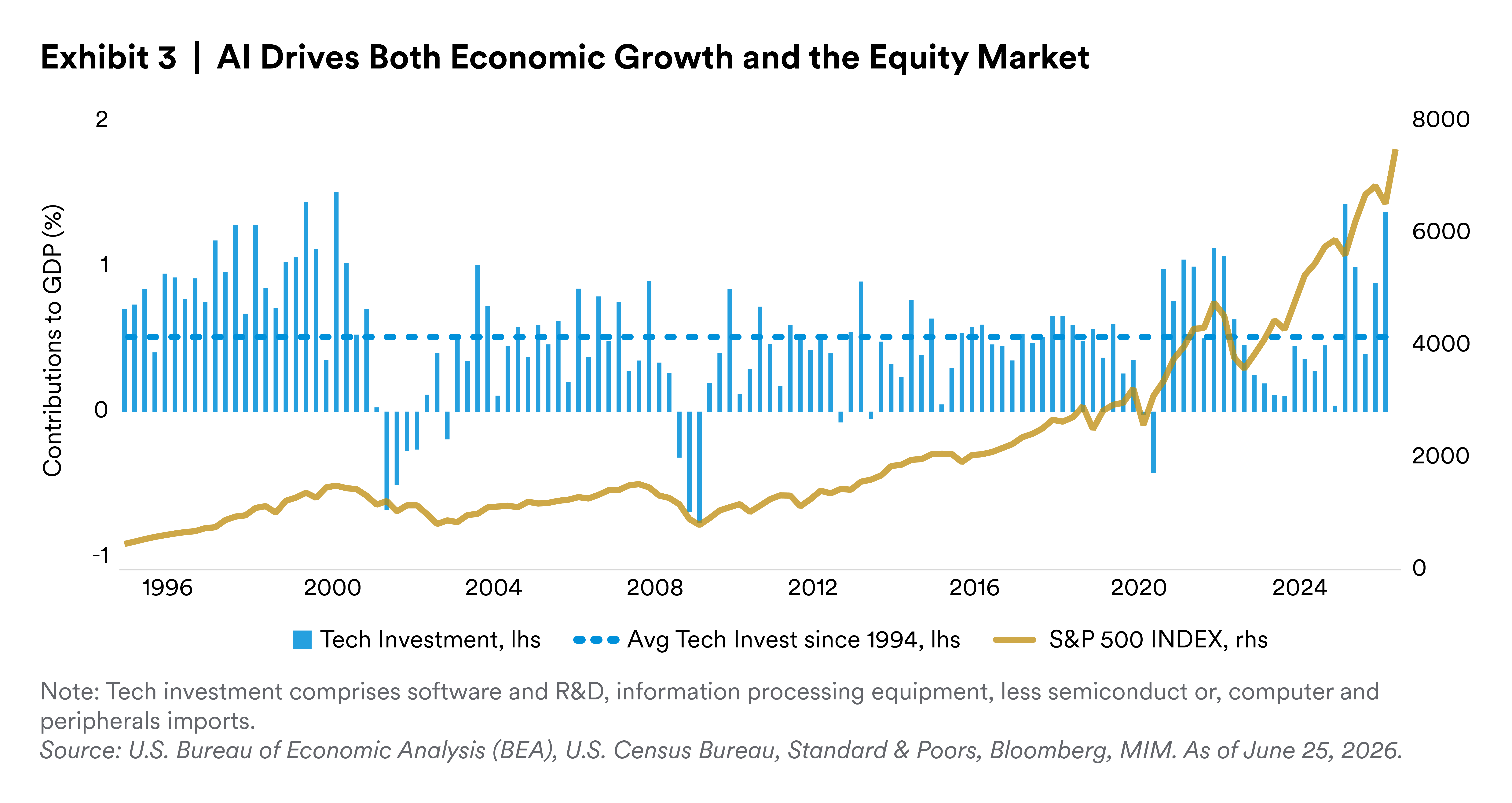

This scenario assumes a continued AI boom in the U.S. (Exhibit 3). But an acceleration of this narrative would raise our concerns around the inflationary effects of AI over the next 6-to-18 months. First, materials costs are likely to rise. The buildout of AI hardware and data centers requires materials that are needed in other products, and we are concerned about spillover effects on prices from the high demand. This includes everything from the most obvious items, semiconductors, to less obvious ones, such as building materials. Second, services costs such as construction and utilities are also likely affected.

A second-order effect is the consumption driven by the AI-equity boom. The resulting wealth effect has driven consumer spending but has the potential to tip over into inflationary spending.

Prices for AI-related inputs have risen but have been somewhat ignored due to the attention-grabbing price effects of the Strait of Hormuz closures. Indeed, inflation may not rise as sharply as it did with the Iran conflict but would continue on a slow burn.

Key implications: This presents a classic overheating scenario. Inflation would remain stubbornly high into the medium term, even as the AI boom persists. To reconverge toward the Warsh-reaffirmed 2% target, the Fed would need to hike rates eventually, although in this scenario it would be pushed off to 2027. The 10-year Treasury could rise via two separate forces: elevated inflation expectations as convergence is pushed out and continued positive expectations around AI leading to greater real growth over the long run. Policy rates would diverge as Fed Funds are hiked.

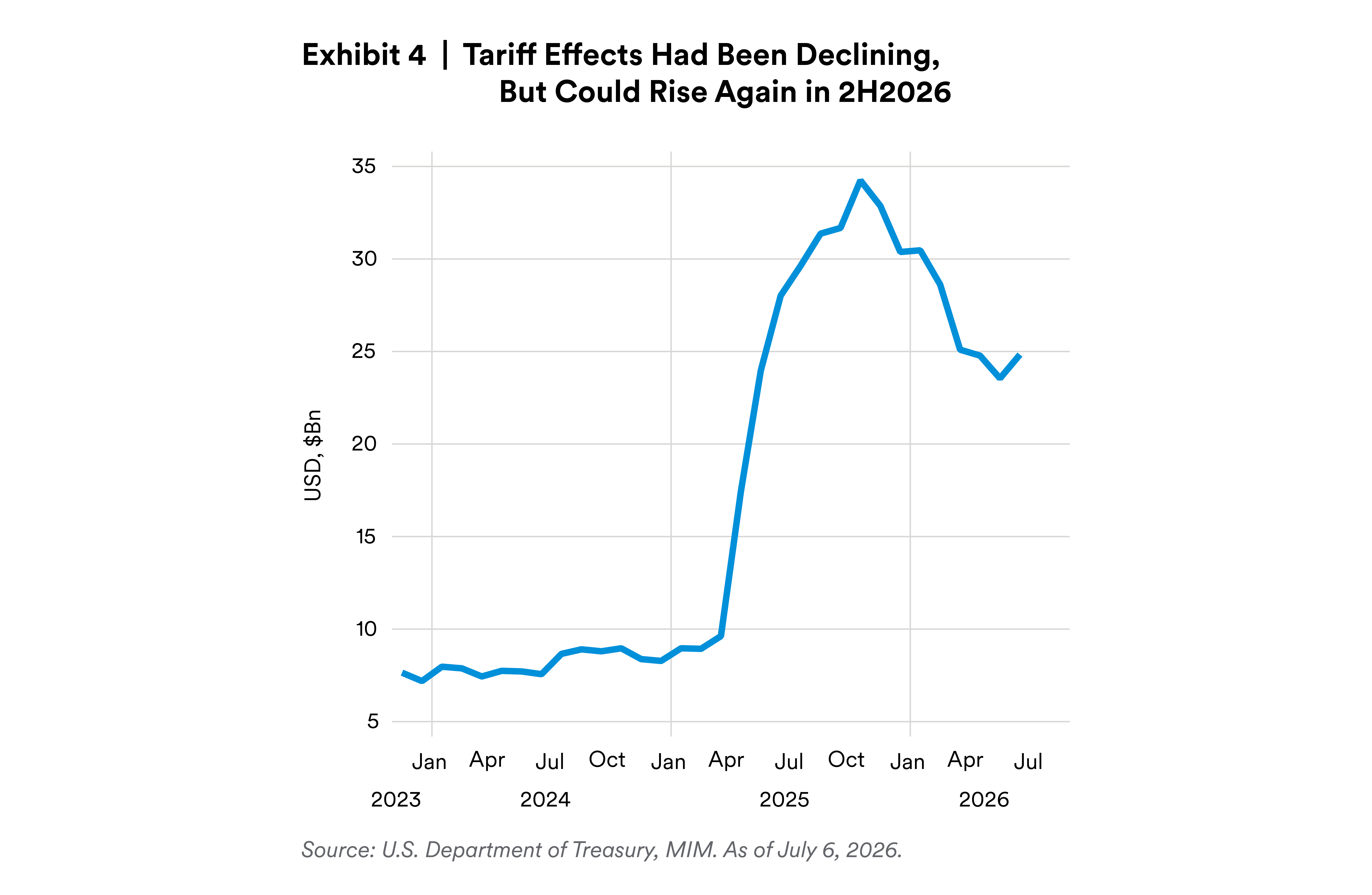

We expect tariffs to once again rise in economic significance in the second half of the year (Exhibit 4). The Trump Administration is preparing to implement a new wave of more durable tariffs. The key risk is that the tariffs come in substantially higher than expected and are volatile despite the more legalistic approach.

The 10% tariffs applied under Section 122 are set to expire on July 24, 2026. Tariffs implemented under Section 122 are intended to be temporary, and we expect the administration to implement more permanent tariffs under Section 301 immediately upon their expiry. While the magnitude of the Section 301 tariffs is expected to be similar to their Section 122 counterparts (10%-12.5%), another wave of negotiations with trade counterparties and legal challenges could arise. This is especially true for countries where new tariffs may stack with existing tariffs. Legally, Section 301 tariffs are more durable than the Liberation Day tariffs because they undergo an investigative process: The administration is conducting investigations on the use of forced labor and structural excess capacity on imports to determine the products to which the tariffs can apply.

Additionally, the U.S. has declined to renew the United States-Mexico-Canda Agreement (USMCA) by July 1, meaning greater uncertainty, as the agreement is subject to annual review for the next 10 years.

Within the U.S., these uncertainties mean businesses will face another spike of policy uncertainty. Navigating rule changes is especially difficult for smaller businesses that have fewer financial and legal resources than large firms. Depending on the size and duration of any ultra-high tariffs, there could be renewed inflation impulses filtering through the economy. We would expect only modest negative effects on growth as there are significant growth impulses elsewhere in the economy that are likely to be indifferent to tariffs.

Internationally, we could see renewed uncertainty in supply chains, especially in countries where Section 301 tariffs come on top of existing tariffs. Expiring provisions of previous negotiations could compound these effects. For example, China has tariff exclusions for 164 different products that are expiring on November 29.

Key implications: Market volatility is likely to be substantially more muted than under Liberation Day tariffs. Markets have become somewhat immune to tariff shocks; indeed, many firms have seen widening profit margins since Liberation Day. There would, however, still be inflation effects, likely replicating the relatively long tail of price increases that resulted from Liberation Day tariffs. Similarly, foreign firms have likely adapted defensively to the repeated possibilities of U.S. tariff hikes. Finally, the EU remains exceptionally vulnerable to new tariffs through its open economy, substantial bilateral trade with the U.S., and China trade. China may redirect its export pressure toward Europe if it negotiates successfully with the U.S. Europe likely has insufficient geopolitical leverage or domestic cohesion to mount a coordinated response.

Elevated tariffs are likely to mean a higher inflation hill to climb for the FOMC, but only marginally so relative to its already elevated inflation troubles. Globally, re-elevated U.S. inflation would most likely present as a slight downward pressure on growth.

There are numerous fragile sources of demand propping up the global economy that could individually or jointly fail.

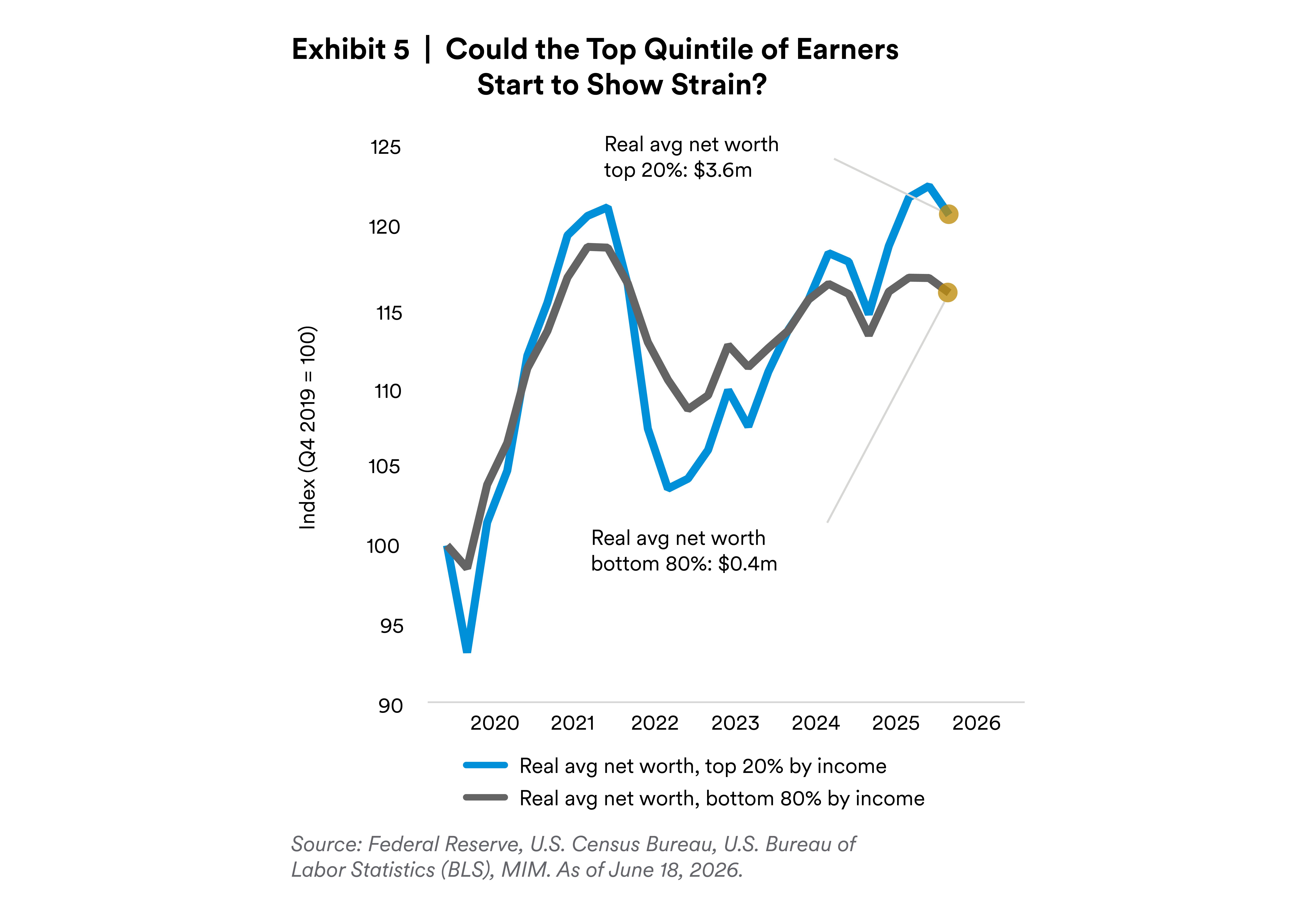

U.S. consumers were struggling even before the Iran conflict sent oil prices surging. They have contributed only 0.86 percentage points to GDP growth, compared to the long-run average contribution of nearly 2 percentage points. The top 20% of consumers have mostly done well, but there are risks that consumer weakness expands to include some part of that group (Exhibit 5). This could arise from increasing worries and cautious attitudes, particularly if the inability to find employment or switch jobs are added to affordability worries.

In much of Europe, oil-importing emerging markets and China, there have been signs of weakening demand. In Europe, weaker-than-expected government demand has coincided with a more stressed consumer. In Germany, fiscal stimulus has occurred at a sluggish pace. France presents similar vulnerabilities, with the government’s restrained fiscal response to a Q1 contraction leaving households disproportionately exposed to the income squeeze. Government spending in Italy, as the most-exposed large Eurozone economy, is constrained by a high debt-to-GDP ratio and the country’s Excessive Deficit Procedure.

Key implications: Cuts begin to be a more palatable option for the FOMC if consumer pullback reduces inflation pressure. Decelerating inflation is not inevitable, especially if the AI sector remains buoyant. Elements of stagflation, with the Fed caught between economic weakness and elevated inflation, become more likely in this scenario. Spillovers globally may be modest but could at the margin reduce support for vulnerable European and Chinese growth. In the Eurozone, sufficient falling demand could reduce pressure on the ECB to raise rates, which optimistically would provide relief to borrowing and valuations.

Concerns around the high valuations in U.S. markets have so far not been validated, and we do not expect a sharp correction in 2026. Markets are seeing sufficient evidence of the importance and applicability of AI to continue funding various forms of AI adoption. There is, moreover, the global competitiveness and national security drivers underlying the U.S. drive to adopt AI. However, corrections can arise unexpectedly, and we expect that some AI-related firms will ultimately prove to be overvalued. AI may start to claim casualties among legacy firms that are challenged by more nimble AI-embracing competitors, unsuccessful AI-native startups, or small businesses that cannot finance proper adoption. Bankruptcies and layoffs could follow. Investment flows in AI buildouts, as well as IPOs and bond issuance all become relatively scarce.

A prolonged market correction would undermine the spending of the top 20% of households – many of whose spending power is substantially tied to their ability to meet saving and wealth preservation goals. A sharp increase in layoffs – somewhat less likely given the lack of expansionary hiring over the last few years – would even more substantially undermine consumption. However, the slow hiring environment means that workers are increasingly anxious about layoffs and may reduce spending out of an abundance of caution.

Key implications: This would be a relatively clear-cut scenario for an economic downturn, if not a recession. A collapse in both AI spending and consumer spending would very likely reduce inflation and clear a path to a Fed cutting cycle.

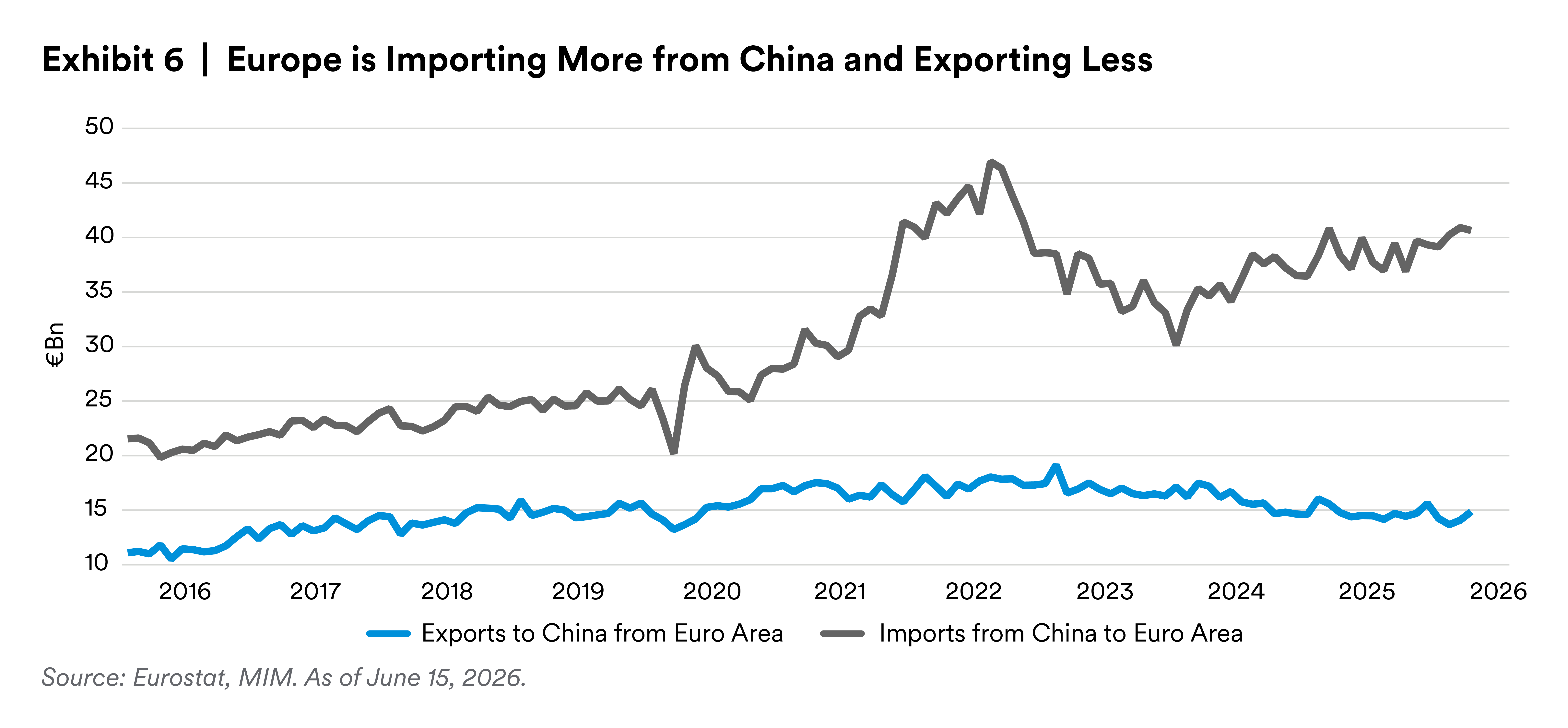

A key geopolitical risk is the changing relationship between the EU and China, particularly with respect to trade. The EU's relationship with China has entered a new and more adversarial phase. Most important is the design of any trade measures taken by the EU. Until now, the EU has remained broadly open to Chinese manufactured goods even as the United States became more restrictive. A shift in EU policy would push the global economy one step farther away from the post-WWII international order.

What was once framed by Brussels as manageable trade friction is now characterized as a macroeconomic shock, with industry commissioner Stéphane Séjourné warning — with more than a little exaggeration — that 29 million EU manufacturing jobs face an existential threat from Chinese overproduction.

On the Chinese side, we expect that Beijing, having weathered Trump's Liberation Day tariffs with relative confidence, will keep its response calibrated and reactive rather than preemptive. It can rely on its expanded toolkit of rare earth restrictions, targeted trade investigations and its newly invoked anti-extraterritoriality instrument3 to raise the cost of escalation for Europe.

China’s export power and expanded policy toolkit for Europe are more nuanced than the prevailing alarm suggests.

China’s export power and expanded policy toolkit for Europe are more nuanced than the prevailing alarm suggests. The deterioration in Europe’s bilateral trade balance with China bilateral balance has been almost entirely offset by an expansion in the surplus with all other trading partners. Moreover, export unit values have risen faster than volumes, suggesting retained pricing power rather than competitive retreat.

The most underappreciated dimension of this scenario is that the surge in EU imports from China is dominated not by intermediate and capital inputs — electronic components, machine parts, and auto parts representing some €130 billion annually. Their falling prices have provided EU manufacturers with a meaningful route to margin recovery.

Key implications: Under this scenario, an increase in tensions could ensnare other open economies and pose a near-term negative for EU growth due to China’s considerable capacity to inflict economic damage. Exposure by third countries to the threat of an EU shift toward less open trade would be a concern, as would exposure to highly volatile discretionary purchases in the EU.

Our baseline scenario assumes that the fragile U.S.-Iran diplomatic track will remain on course following the signing of the Memorandum of Understanding in June. The process is likely to be noisy at points, with possible tit-for-tat flare-ups and extensions to the 60-day period. Normalization of traffic volume in the Strait of Hormuz is expected to be gradual and highly dependent on diplomatic stability. We expect that Iran will continue to try to assert control over the Strait of Hormuz unilaterally, with de facto tolls and recognition via the Persian Gulf Strait Authority (PGSA).

We see downside risks of Iran, Israel, and/or the U.S. overplaying their hands. Hardline elements of the Iranian regime would gain traction in their narrative of strategic leverage and achievements to date. Under this scenario, Iran would insist on a ceasefire in Lebanon, a pause of the MoU, and/or reclosing the Strait for an extended period. For Israel, domestic politics and national security concerns could override pressure from the U.S., particularly given the Knesset election this year with polling looking uncertain for Netanyahu amidst criticism of little-to-no strategic gains since October 2023. For the U.S., vindication for the Iran hawks in the administration over Iran’s untrustworthiness could bring military action back on the table.

Key implications: Sharp inflation acceleration would be back on the table, particularly in oil prices. This could trigger a reprise of the market scenario that prevailed from March to May 2026, with already stressed consumers and diminished national reserves accelerating the impact.

We see the key upside risk as a rapid and superficial agreement, fed by a desire by both the U.S. and Iran to save face and put the conflict behind them. With the U.S. and Iran wanting to avoid a resumption of full-scale conflict, an upside scenario could come from mechanisms that allow parties to claim they have achieved their objectives. Under pressure from China and India, Iran could agree to morph the Persian Gulf Strait Authority (PGSA) into a Joint Maritime Security Council in cooperation with the U.S., Oman, and the GCC states. This would allow the U.S. to preserve freedom of navigation under international law while giving Tehran a legal stake in the Strait. Similarly, face-saving frameworks on nuclear discussions could be achieved via a commercial swap of Iran’s highly enriched uranium stockpile. These mechanisms would lead to a permanent deal more quickly than expected, allowing for a material reduction in uncertainty and faster normalization in oil-and-gas flows.

Key implications: Faster resolution to oil supplies, faster convergence of cargo traffic, lower prices for passage. This would represent broadly going back to the status quo ante with the potential economic benefit of getting more Iranian oil into the global economy.

Aside from economic vulnerabilities of the Eurozone, there are renewed stresses within the Eurozone area. Germany faces the most acute structural deterioration, with two consecutive negative GDP prints expected in 2Q26 and 3Q26. Political fragmentation, including anticipated gains for the right-wing AfD party in September state elections, constrains the room for supply-side reform.

In France, the April 2027 presidential election introduces a political risk premium that can no longer be treated as tail risk. A right-wing Rassemblement National (RN) victory in France would not be an outright rupture: The party has abandoned Frexit, and France's institutional architecture of Senate, Constitutional Council, and financial market discipline would act as powerful checks. However, its fiscal platform is heavy on costly pledges, and financial markets — already nervous about French debt — would likely push French borrowing costs further above Germany's.

Italy’s economic stress during the Iran conflict has been particularly acute. It is the most energy-exposed large economy in the Eurozone and has a very high debt-to-GDP ratio. Households need relief, but the government has limited capacity to provide it. Its near-140% debt-to-GDP ratio means any rise in borrowing costs hits the budget with immediate force. Any sharp widening in Italian spreads would reawaken Eurozone fragmentation risk.

Key implications: We do not see Eurozone fragmentation as a significant risk scenario. However, weakness in large member countries could raise political and market concerns. This could widen spreads, weaken Eurozone markets at large, and influence election outcomes.

We do not expect significant economic effects from the U.S. midterms. Economic shifts largely emanate from one party gaining or retaining control of the presidency and both houses of Congress. The base case, according to polling and election watchers, is for Democrats to gain control of the House of Representatives. The risk scenario would therefore be a Republican sweep of the House and Senate.

Key implications: A Republican sweep of Congress could inject new fiscal uncertainty into the mix. Congress would retain the ability to pass Republican priorities. The threat of a debt-ceiling crisis would be elevated relative to the base case, given the greater power of fiscal hawks in the Republican caucus. Policy may become more stable, as a sweep would give President Trump more time and latitude to consolidate his policy stances in areas such as trade, immigration, and AI.

Our base case shows a global economy in recovery from a severe oil shock. Inflation is elevated but not as much as in the post-pandemic inflation shock. Global growth has been hurt, but the largest economies have escaped the dire predictions of the early days of the conflict. The U.S. economy has continued its solid growth, carried largely by AI investment.

We expect inflation risks to moderate over time globally, and hike expectations in the U.S. to disappoint. We further expect the AI boom to carry on through year-end. Nevertheless, we remain alert to persistent or new inflation threats. We do not take global demand strength for granted and note its fragility. Finally, geopolitical risks remain substantially elevated as a now-perennial wild card.

Endnotes

1 Bloomberg Intelligence. “Deep Dive: Gen AI’s Need for Speed Fuels Accelerator Chip Market.” January 11, 2026.

2 Bloomberg Intelligence. “AI Spending on Pace to Near $5 Trillion Through 2030.” June 1, 2026.

3 Beijing has invoked a newly announced anti-extraterritoriality framework in the context of an EU investigation into a Chinese security-screening firm. This framework bars entities in China from cooperating

Disclosure

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors.

MetLife Investment Management (MIM), which includes PineBridge Investments, is MetLife Inc.’s institutional investment management business. MIM is a group of international companies that provides investment advice and markets asset management products and services to clients around the world.

This document is solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

The various global teams referenced in this document, including portfolio managers, research analysts and traders are employed by the various legal entities that comprise MIM.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results.

In the U.S: This document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities and Exchange Commission (SEC) registered investment adviser. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment adviser.

For investors in the UK: This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address One Angel Lane 8th Floor London EC4R 3AB United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK who qualify as a "professional client" as defined under the Markets in Financial Instruments Directive (2014/65/EU), as per the retained EU law version of the same in the UK.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Investment Management Japan, Ltd. (“MIM JAPAN”), a registered Financial Instruments Business Operator (“FIBO”) conducting Investment Advisory Business, Investment Management Business and Type II Financial Instruments Business under the registration entry “Director General of the Kanto Local Finance Bureau (Financial Instruments Business Operator) No. 2414” pursuant to the Financial Instruments and Exchange Act of Japan (“FIEA”), and a regular member of the Investment Management Association of Japan and the Type II Financial Instruments Firms Association of Japan. In its capacity as a discretionary investment manager registered under the FIEA, MIM JAPAN provides investment management services and also sub-delegates a part of its investment management authority to other foreign investment management entities within MIM in accordance with the FIEA. This document is only being provided to investors who are general employees' pension fund based in Japan, business owners who implement defined benefit corporate pension, etc. and Qualified Institutional Investors domiciled in Japan. It is the responsibility of each prospective investor to satisfy themselves as to full compliance with the applicable laws and regulations of any relevant territory, including obtaining any requisite governmental or other consent and observing any other formality presented in such territory. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

For Investors in Hong Kong S.A.R.: MetLife Investment Management and PineBridge Investments operate through the following entities: MetLife Investments Asia Limited (“MIAL”), licensed by the Securities and Futures Commission (“SFC”) for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities, PineBridge Investments Asia Limited licensed by the SFC for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities, and PineBridge Investments Hong Kong Limited licensed by the SFC for Type 1 (dealing in securities) and Type 9 (asset management) regulated activities. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are licensed by the SFC to carry on regulated activities in Hong Kong S.A.R. The information contained in this document is for information purposes only and it has not been reviewed by the Securities and Futures Commission. This document may also be distributed by certain PineBridge Investments affiliates acquired by MetLife Investment Management on December 30, 2025. For additional legal and regulatory disclosures including other cross border information, please refer to https://www.pinebridge.com/en/regulatory-disclosure.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

For investors in the EEA: This document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. The investment strategies described herein are directly managed by delegate investment manager affiliates of MIMEL. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are directly contracted with MIMEL or are regulated in Ireland. Unless otherwise stated, any industry awards referenced herein relate to the awards of affiliates of MIMEL and not to awards of MIMEL.